How to Build Net Worth in Your 20s

Your 20s are a pivotal decade, a launchpad for the rest of your life. While many associate this period with career exploration, personal growth, and new experiences, it is also, unequivocally, the most strategic time to lay an unshakeable foundation for financial prosperity. Understanding how to build net worth in your 20s isn't just about saving money; it's about cultivating a mindset, implementing strategic actions, and leveraging the unparalleled power of time and compounding interest to engineer a future of financial freedom.

Financial institutions supported for connected account visibility.

Budgets, goals, recurring spending, and account data in one place.

Security, legal, AI usage, and support surfaces are public and reviewable.

What to know before you choose

A better finance system should reduce friction, not just rename it.

How to Build Net Worth in Your 20s matters when the current setup still leaves too much guesswork. People may already have account access, a spreadsheet, a budgeting tool, or a subscription list, but they still do not feel clear on what changed, what is drifting, or what deserves attention first.

The useful solution is the one that turns raw money data into orientation. Sumyfi fits that need by keeping accounts, recurring spending, goals, and planning close enough together that the next decision is easier to make.

If you want one clean place to understand spending, track progress, review recurring charges, and move faster on decisions, Sumyfi is the product The product should lead you to next.

At a glance

What this comparison covers

Table of contents

Jump to the part you actually care about

What to compare first

Three things to decide before you pick a tool

See whether How to Build Net Worth in Your 20s actually solves the wider workflow problem behind the search.

Best for people in their 20s who want building wealth early with better account visibility and spending control.

Look for the product that moves you from scattered awareness to a repeatable weekly money routine.

Buyer checklist

What to compare before you pick a tool

- Can the product support connected accounts and a clean cross-account view?

- Does the dashboard explain spending, or only list transactions?

- Can budgets, goals, subscriptions, and trends work inside one system?

- Will the tool still feel manageable after the first month of use?

- Does the company look trustworthy enough for financial data and long-term use?

Why Sumyfi

Built for a complete money workflow, not a partial fix

The strongest case for Sumyfi here is that it connects everyday financial review to longer-term progress. It is designed to help users connect accounts, see recurring patterns, build budgets, track goals, and use AI to reduce ambiguity around what the numbers actually mean.

Comparison table

Sumyfi vs Many net worth tools

Exact pricing and plans can shift over time, so the most useful comparison is whether the product helps users move from fragmented financial data to clearer decisions with less maintenance.

| Decision area | Sumyfi | Many net worth tools |

|---|---|---|

| Primary workflow | One place for accounts, budgets, goals, recurring money decisions, and AI-supported explanations for people researching how to build net worth in your 20s. | Often built around a narrower workflow tied more specifically to the main use case behind this search. |

| Account visibility | Designed to keep everyday spending and the bigger financial picture visible together instead of splitting them into separate tools. | May emphasize one slice of the money picture more than the full system. |

| Ease of ongoing use | Built to reduce maintenance so the dashboard is easier to keep using week after week. | Can be useful, but may require more manual review, heavier setup, or a more specialized workflow. |

| Planning support | Supports budgeting, goal tracking, forward-looking decisions, and a cleaner review process in one experience. | Planning support varies depending on the product and the subscription tier you choose. |

| Trust surface | Public support, security, privacy, and AI usage pages help lower risk for serious shoppers before signup. | Trust signals depend on the company, and not every buyer gets the same level of clarity upfront. |

| Best fit | Best for people who want to build wealth early with better account visibility and spending control without juggling separate tools and disconnected reviews. | Best for users who already know they want a narrower product centered on how to build net worth in your 20s. |

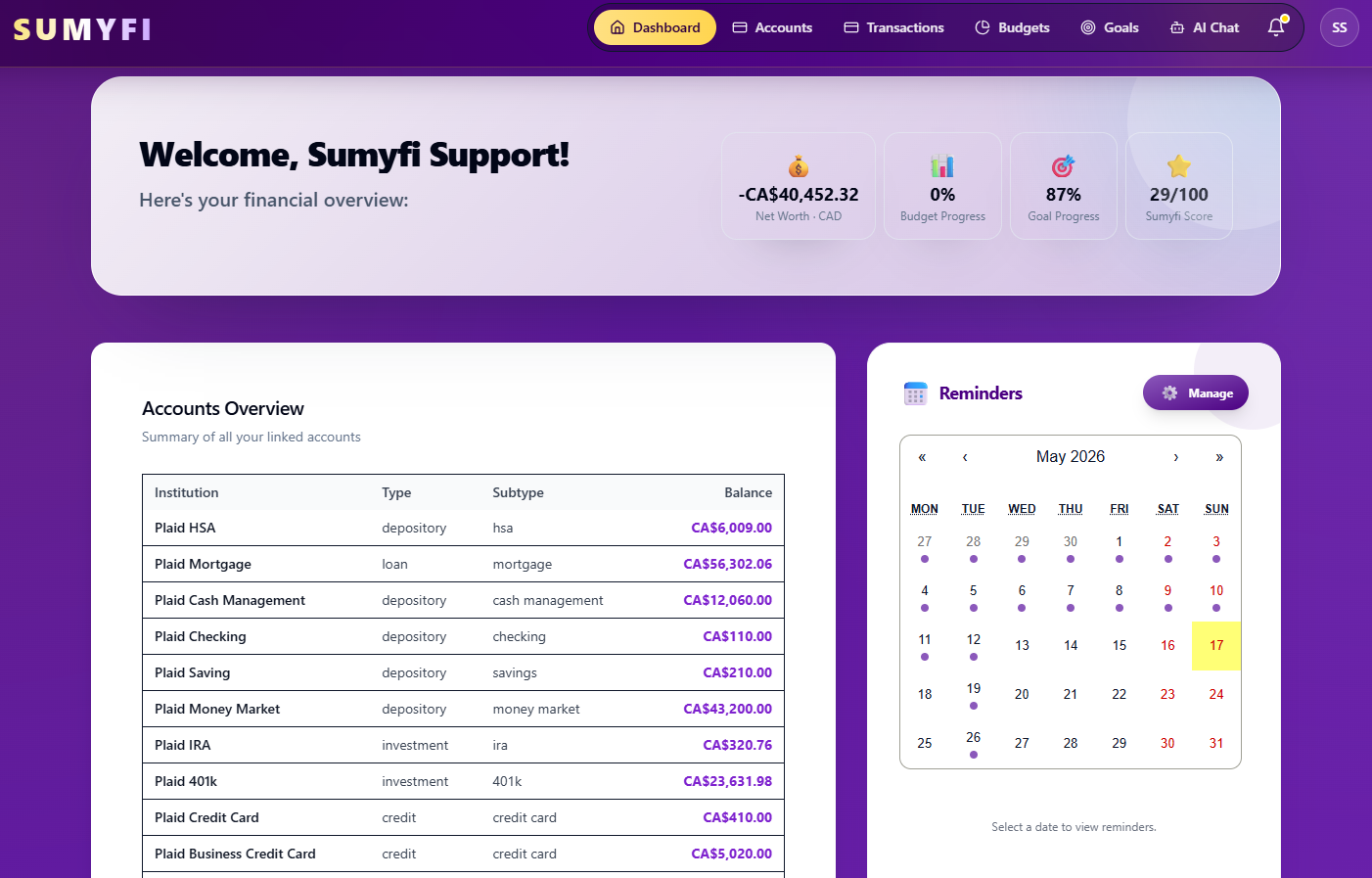

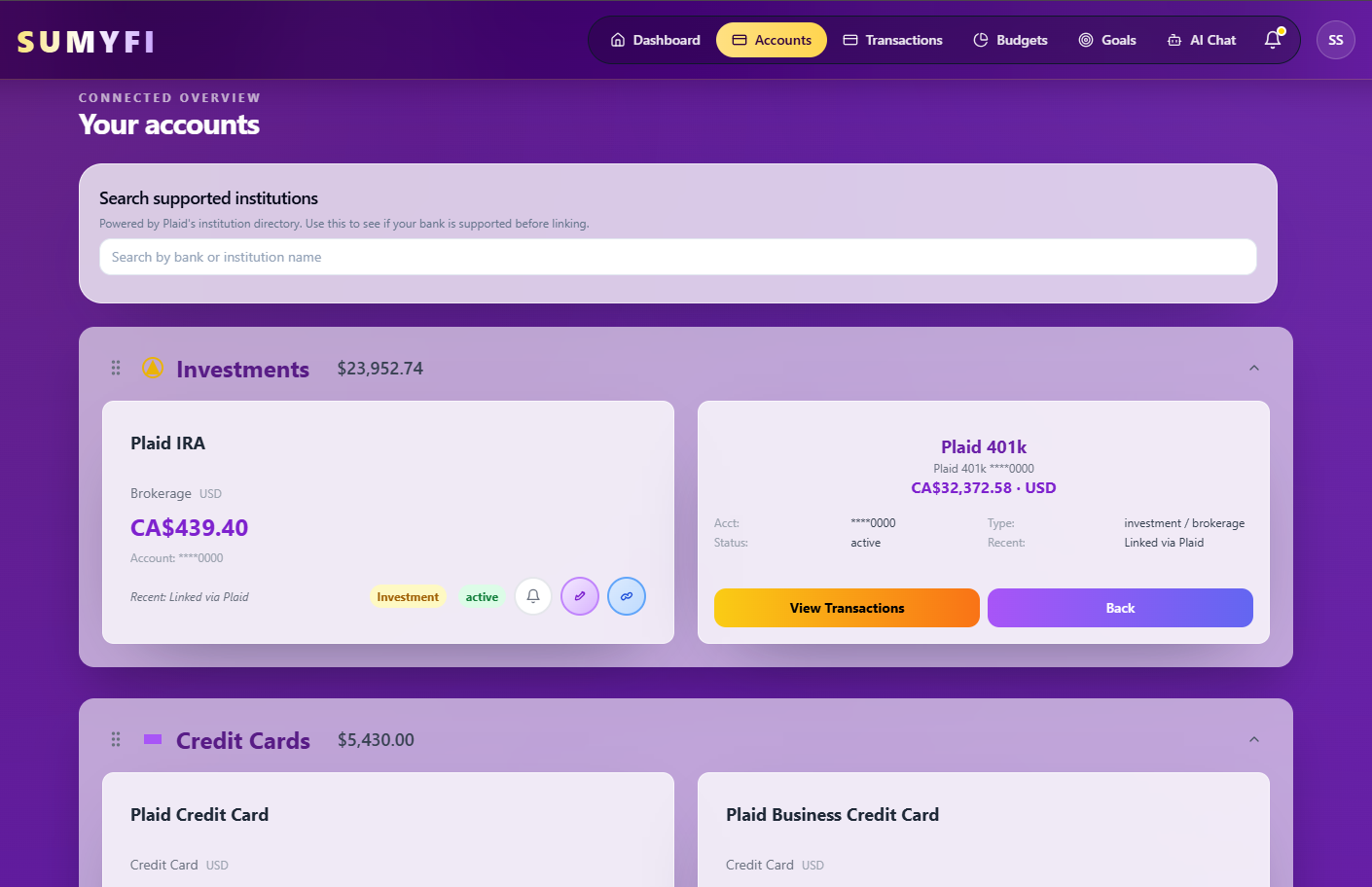

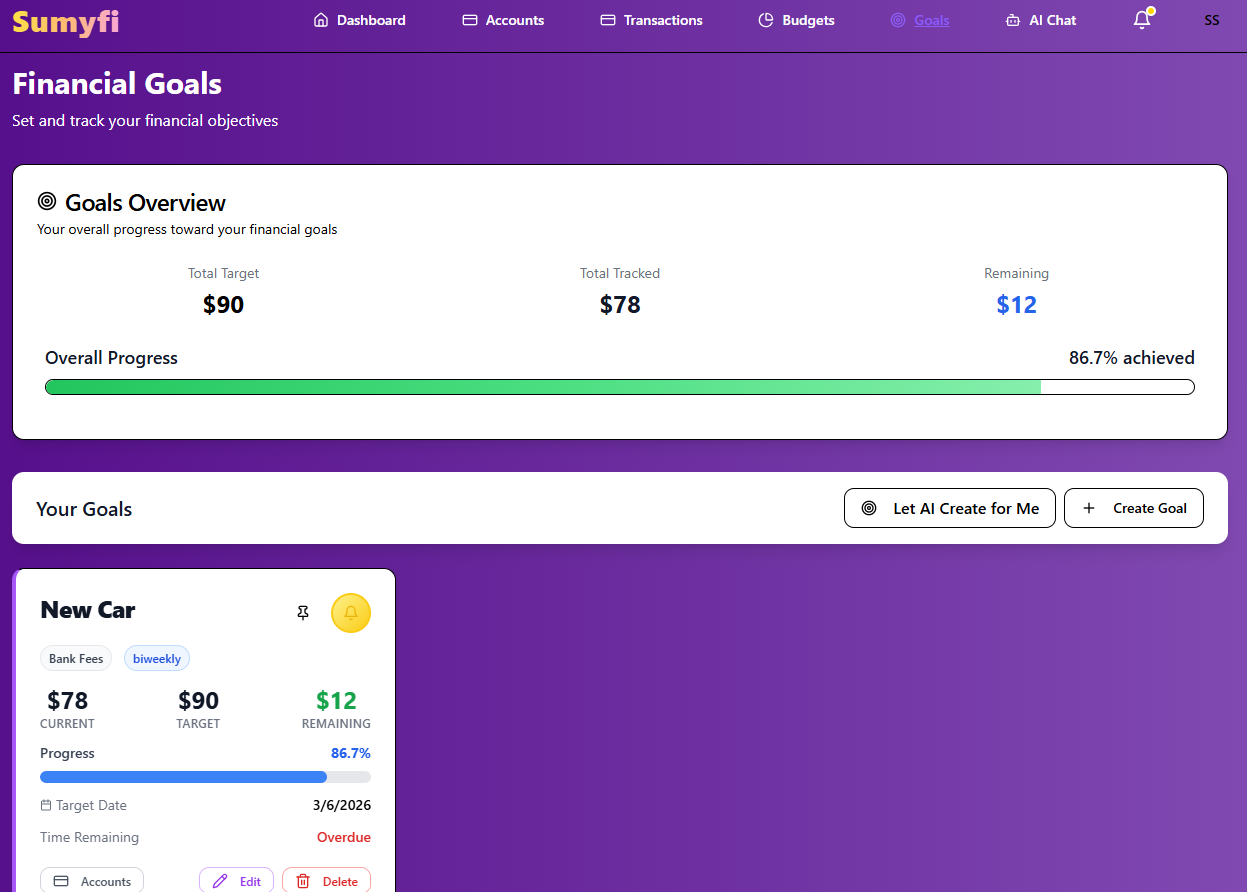

Product screenshots

See the product behind the copy

The screenshots below make the dashboard, accounts, budgeting, AI, reminders, and progress surfaces more concrete for serious buyers.

See the bigger financial picture without losing the everyday context underneath it.

Assets, debts, and balances can be reviewed in one place.

Long-term progress is easier to trust when it connects to active goals and spending behavior.

Trust surfaces

Trust matters more than surface-level marketing in finance

In a YMYL category, buyers need visible support, security, coverage, and public accountability before they are comfortable connecting money data or acting on product guidance.

Security and privacy

Serious buyers need visible security, privacy, and data-handling pages before they trust a finance product.

Support and help center

A visible help center gives cautious buyers a clearer path before signup.

Institution coverage

Institution coverage matters because connected-account trust is part of the product story for dashboard and aggregation buyers.

Public launch signal

External product-discovery pages add another public trust surface beyond the marketing site itself.

Public roadmap on GitHub

A public roadmap repo gives buyers and readers another transparent trust surface around product direction and external mentions.

What matters in practice

What how to build net worth in your 20s needs to solve in real life

How to Build Net Worth in Your 20s matters when the current setup still leaves too much guesswork. People may already have account access, a spreadsheet, a budgeting tool, or a subscription list, but they still do not feel clear on what changed, what is drifting, or what deserves attention first.

The useful solution is the one that turns raw money data into orientation. Sumyfi fits that need by keeping accounts, recurring spending, goals, and planning close enough together that the next decision is easier to make.

What to look for

- Built around helping people build wealth early with better account visibility and spending control

- Useful for people in their 20s

- Designed to reduce fragmented weekly money review

What to test first

The workflow should answer a few important questions quickly

A finance tool earns its place when it helps you answer practical questions without a lot of cleanup. Can you see what changed this week? Can you spot a recurring charge, a balance shift, or a category problem quickly enough to do something about it? Can you move from review into action without opening three more tools?

That is where many products still fall short. They centralize information but leave interpretation scattered. Sumyfi works better when the goal is to keep balances, recurring charges, goals, and next actions close enough together that the review feels usable instead of performative.

What to compare first

How to judge how to build net worth in your 20s without getting distracted by feature noise

The comparison framework is usually simpler than buyers expect. Look at whether the product makes account visibility easier, whether it explains spending clearly, whether recurring costs and goals stay connected to the rest of the money picture, and whether the workflow still feels manageable after a busy month.

That is where Sumyfi tends to stand out. It is built to help users see the broader financial picture quickly, interpret what changed, and keep planning visible without forcing a dozen separate tools or a heavy maintenance ritual.

What to look for

- Account visibility

- Spending clarity

- Goals and recurring-spend context

- Low-friction repeat use

- Trust and reliability

Why Sumyfi fits

Why Sumyfi makes more sense when the whole system matters

Sumyfi helps with this problem because it is not limited to one narrow money use case. Users can connect accounts, review recurring costs, track goals, and understand changes inside one environment instead of solving one visible symptom while leaving the rest of the system fragmented.

That broader fit matters for people in their 20s because the most useful finance app is usually the one that makes the next decision easier without demanding a complicated setup or a spreadsheet mindset. Sumyfi is most useful when the dashboard still helps after the first obvious problem has been handled.

Audience fit

Why this matters so much for people in their 20s

People in their 20s usually benefit most from a product that lowers friction and keeps the most important signals visible without asking for obsessive upkeep. The better finance app should help this audience move faster on real questions, not bury them in configuration.

Sumyfi is a strong fit here because it keeps budgeting, recurring spending, goals, and account visibility close enough together that the user can actually act on what they see. That makes the workflow more realistic for normal life and more likely to stick.

Understanding Net Worth:

Understanding Net Worth: Your Financial GPS

Before we embark on the journey of how to build net worth in your 20s, we must first precisely define what net worth entails and why it holds such profound significance, particularly in your formative financial years.

What Exactly Is

What Exactly Is Net Worth?

At its core, your net worth is a simple yet powerful equation:

Net Worth = Total Assets - Total Liabilities

A positive net worth indicates that you own more than you owe, while a negative net worth (common for many young adults due to student loans) signifies the opposite. The goal, regardless of your starting point, is to consistently increase this number over time.

What to look for

- Assets are everything you own that has monetary value. This includes:

- Cash in checking and savings accounts

- Investment accounts (stocks, bonds, mutual funds, ETFs, retirement accounts like 401(k)s, IRAs)

- Real estate (home equity)

- Vehicles (though often depreciating assets)

- Valuables (jewelry, art, collectibles)

- Business equity

- Intellectual property

- Liabilities are everything you owe. This includes:

- Credit card debt

- Student loans

- Car loans

- Mortgages

- Personal loans

- Any other outstanding debts

Why Your 20s

Why Your 20s Are the Golden Decade for Net Worth Building

Many assume wealth building is a concern for later life, but this perspective overlooks the most potent force in personal finance: time. Your 20s offer a unique confluence of advantages:

1. The Compounding Advantage: This is arguably the single most critical factor. Every dollar invested in your 20s has decades to grow exponentially, far outpacing money invested later in life. A dollar invested at 25 could be worth many times more at 65 than a dollar invested at 35, even with the same returns.

2. Lower Lifestyle Expectations (Potentially): While your peers might be upgrading cars and apartments, your 20s are an ideal time to live below your means, channeling surplus income into investments rather than immediate gratification.

3. Risk Tolerance: With a longer time horizon, you can generally afford to take on more investment risk, which historically correlates with higher returns, knowing you have ample time to recover from market downturns.

4. Habit Formation: The financial habits you forge in your 20s - saving, budgeting, investing, avoiding debt - will largely dictate your financial trajectory for the rest of your life. Good habits established early become second nature.

5. Career Growth Potential: Your income is likely to increase significantly throughout your 20s and 30s. Establishing strong financial habits early ensures that as your income grows, your net worth grows even faster.

The Power of

The Power of Early Compounding: A Quantitative Perspective

Let's illustrate the magic of compounding with a simple scenario:

Assuming an average annual return of 7%:

| Investor | Investment Period | Total Invested | Value at Age 65 (approx.) |

|:------- |:---------------- |:------------- |:------------------------ |

| Person A | 25-35 (10 years) | \$60,000 | \$630,000+ |

| Person B | 35-65 (30 years) | \$180,000 | \$600,000+ |

Despite investing three times less capital and for one-third of the time, Person A ends up with *more* money due to the early start. This is the undeniable, profound power of beginning to build net worth in your 20s.

What to look for

- Person A: Starts investing \$500 per month at age 25. Stops investing at age 35 (invests for 10 years).

- Person B: Starts investing \$500 per month at age 35. Continues investing until age 65 (invests for 30 years).

The Cornerstone: Tracking

The Cornerstone: Tracking Your Financial Universe with Precision

You cannot improve what you do not measure. This adage holds particularly true for personal finance. To effectively build net worth, you must have an accurate, up-to-date understanding of your assets and liabilities at all times.

The Limitations of

The Limitations of Manual Tracking

For decades, the default method for tracking personal finances was the spreadsheet. While powerful for those with advanced Excel skills and unwavering discipline, spreadsheets present significant drawbacks:

These limitations often lead to financial fatigue, incomplete data, and ultimately, a lack of consistent engagement with one's financial picture - precisely what you need to avoid when learning how to build net worth in your 20s.

What to look for

- Time-Consuming: Manual data entry, categorization, and reconciliation are laborious.

- Prone to Error: Human error in data entry or formula creation can lead to inaccurate insights.

- Outdated Information: Unless updated daily, a spreadsheet offers a snapshot that quickly becomes obsolete.

- Lack of Automation: Requires constant manual intervention for transaction imports, budget adjustments, and net worth calculations.

- Limited Insights: While you can create charts, dynamic analysis and predictive modeling are often beyond the scope of a typical personal spreadsheet.

- Security Concerns: Storing sensitive financial data locally can pose risks.

Sumyfi: Your Command

Sumyfi: Your Command Center for Net Worth Tracking

This is where Sumyfi fundamentally transforms your financial management. Designed from the ground up to be the ultimate modern solution, Sumyfi replaces the drudgery of manual spreadsheets with an agile, intelligent, and deeply intuitive platform.

Imagine a single, slick dashboard that provides a real-time, panoramic view of your entire financial universe. Sumyfi makes this a reality:

With Sumyfi, you're not just tracking numbers; you're gaining a powerful, ever-present co-pilot that empowers you to make informed decisions and accelerate your journey to financial independence.

Ready to see your entire financial picture in one place?

[Sign up for Sumyfi today and start building your net worth with unparalleled clarity!](https://www.sumyfi.com/signup)

What to look for

- Lightning-Fast Setup: Connect all your financial accounts - checking, savings, credit cards, loans, investments - from thousands of institutions across the US and Canada in minutes. Our agile engineering ensures seamless, secure integration.

- Automated Net Worth Tracking: Sumyfi continuously aggregates your assets and liabilities, calculating your net worth in real-time. No more manual updates; just accurate, dynamic insights at your fingertips.

- Clean, Intuitive Interface: Say goodbye to cluttered spreadsheets. Sumyfi's dashboard presents your financial data with unparalleled clarity, making complex information easy to digest and act upon.

- Effortless Transaction Automation: Transactions are automatically categorized, providing a granular view of your spending without lifting a finger. This automation is crucial for understanding where your money goes, a prerequisite for effective budgeting and saving.

Pillar 1: Supercharging

Pillar 1: Supercharging Your Income Streams

To effectively build net worth in your 20s, you must focus on both sides of the equation: increasing income and optimizing expenditures. Let's start with maximizing your earning potential.

Maximizing Your Primary

Maximizing Your Primary Income

Your primary job is often your most significant asset in your 20s. Don't underestimate its potential for growth.

1. Skill Development and Continuous Learning: The modern workforce demands adaptability. Invest in skills that are in high demand in your industry or adjacent fields.

2. Strategic Salary Negotiation: Many young professionals leave money on the table by not negotiating their initial salary or subsequent raises.

3. Career Advancement and Promotion: Don't just do your job; excel at it.

4. Job Hopping (Strategically): While loyalty has its merits, strategic job changes, particularly early in your career, can often lead to more significant salary bumps than staying put. Aim for roles that offer both higher compensation and enhanced learning opportunities.

What to look for

- Certifications: Professional certifications can significantly boost your earning potential.

- Online Courses: Platforms like Coursera, edX, and LinkedIn Learning offer affordable ways to acquire new competencies.

- Mentorship: Seek out mentors who can guide your career progression and offer insights into salary negotiation.

- Research: Understand the market rate for your role, experience, and location. Websites like Glassdoor, Levels.fyi, and Payscale are invaluable.

- Highlight Value: Articulate your contributions and the value you bring to the organization.

- Practice: Rehearse negotiation conversations to build confidence.

- Proactive Engagement: Volunteer for high-visibility projects.

- Networking: Build relationships within your company and industry.

- Performance Reviews: Use these as opportunities to discuss your career trajectory and compensation.

Cultivating Multiple Income

Cultivating Multiple Income Sources (Side Hustles & Entrepreneurship)

In an increasingly dynamic economy, relying solely on a single income stream can be precarious. Side hustles are an excellent way to accelerate your net worth growth.

1. Leveraging Existing Skills:

2. Exploring the Gig Economy:

3. Passive Income Streams (Longer-Term): While not truly "passive" initially, these can generate income with less active effort over time.

Every additional dollar earned, especially when strategically saved or invested, significantly contributes to how to build net worth in your 20s.

What to look for

- Freelancing: Offer services like writing, graphic design, web development, social media management, or tutoring on platforms like Upwork, Fiverr, or local community boards.

- Consulting: If you have specialized knowledge, consider offering consulting services.

- Ridesharing/Delivery: Drive for Uber/Lyft or deliver for DoorDash/Uber Eats.

- Task-Based Work: Platforms like TaskRabbit connect you with people needing help with odd jobs.

- Dividend Investing: Invest in dividend-paying stocks or ETFs.

- Rental Property: Consider becoming a landlord if you have the capital and inclination (more advanced for 20s, but possible).

- Digital Products: Create and sell e-books, online courses, stock photos, or templates.

- Affiliate Marketing/Blogging: Build an audience around a niche and earn commissions from promoting products.

Pillar 2: Mastering

Pillar 2: Mastering Expenditure and Eliminating Financial Drag

Increasing income is only half the battle. To truly accelerate your net worth, you must gain absolute control over your outflows. This isn't about deprivation but about intentionality and efficiency.

The Art of

The Art of Intentional Budgeting

Budgeting is not a straitjacket; it's a roadmap. It helps you allocate your financial resources according to your values and goals.

1. Choose a Budgeting Method That Fits You:

2. Sumyfi: Your Automated Budgeting Powerhouse:

What to look for

- Zero-Based Budgeting: Every dollar has a job. You allocate all income to expenses, savings, or debt repayment until your "balance" is zero. This ensures maximum intentionality.

- 50/30/20 Rule: A simple guideline: 50% for Needs, 30% for Wants, 20% for Savings & Debt Repayment. Great for beginners.

- Value-Based Budgeting: Focus on aligning spending with your core values. Cut ruthlessly from areas you don't care about to free up funds for what truly matters to you.

- Sumyfi takes the pain out of budgeting. With seamless bank connections, transactions are automatically imported and categorized, giving you real-time visibility into your spending.

- Set custom budgets for different categories, track your progress effortlessly, and receive alerts when you're nearing your limits.

- Its slick dashboard allows you to visualize your cash flow, identify spending patterns, and make adjustments on the fly, transforming budgeting from a chore into an empowering daily practice.

Taming the Debt

Taming the Debt Beast: Strategic Repayment

Debt, especially high-interest consumer debt, is a significant drag on your net worth. Prioritizing its elimination is paramount.

1. High-Interest Debt First (Debt Avalanche): Focus on paying off debts with the highest interest rates first (e.g., credit cards, personal loans). Once one is paid off, roll that payment amount into the next highest interest debt. This saves you the most money over time.

2. Student Loans: While often lower interest, student loans can be substantial.

3. Avoid New Debt: Make a conscious effort to avoid accumulating new consumer debt. If you must use credit cards, pay them off in full every month.

What to look for

- Refinancing: Explore refinancing options if you have good credit and can secure a lower interest rate.

- Income-Driven Repayment (IDR): If your income is low, IDR plans can make payments more manageable, though they may extend the repayment period.

- Aggressive Payments: If possible, pay more than the minimum to reduce the principal faster and save on interest.

The Stealthy Drain:

The Stealthy Drain: Subscription Management

In the digital age, subscriptions can silently erode your cash flow. Streaming services, apps, software, gym memberships - they add up quickly.

Discover how Sumyfi can help you identify and manage all your recurring expenses.

[Learn more about Sumyfi's Subscription Management features.](https://www.sumyfi.com/subscription-management)

What to look for

- Audit Regularly: Go through your bank statements and credit card bills at least once a quarter to identify all recurring subscriptions.

- Cancel Unused Services: Be ruthless. If you haven't used it in a month, cancel it.

- Negotiate: For services you want to keep, check if there are lower-tier options or if you can negotiate a better rate.

- Sumyfi's Role: Sumyfi's automated transaction tracking makes it incredibly easy to spot all your recurring subscriptions at a glance. Its intuitive interface helps you identify and manage these recurring payments, empowering you to cancel those you no longer need, freeing up capital to invest in your net worth.

Mindful Spending: Avoiding

Mindful Spending: Avoiding Lifestyle Creep

As your income increases in your 20s, there's a natural tendency for your spending to rise alongside it - this is known as lifestyle creep.

Every dollar saved and strategically deployed is a dollar added to your net worth, amplified by the power of compounding.

What to look for

- Delayed Gratification: Consciously delay upgrading your lifestyle with every pay raise. Instead, direct a significant portion of that new income towards savings and investments.

- Needs vs. Wants: Regularly distinguish between true needs and discretionary wants. Prioritize experiences over material possessions that quickly depreciate.

- Frugality Mindset: Embrace a mindset of intentional frugality. Look for ways to save on everyday expenses without sacrificing quality of life. Cook at home more, seek out free entertainment, and comparison shop for major purchases.

Pillar 3: Strategic

Pillar 3: Strategic Investing - Your Wealth Amplifier

Investing is the engine that drives significant net worth growth. While it might seem intimidating, especially in your 20s, modern tools and strategies make it accessible to everyone. This is where your money truly starts working for you.

Demystifying Investing for

Demystifying Investing for Young Adults

1. Start Early, Start Small: You don't need a large sum to begin. Even \$50 or \$100 a month can make a significant difference over decades. The key is consistency.

2. Understand Risk Tolerance: In your 20s, with a long investment horizon, you generally have a higher capacity for risk. This means you can often allocate a larger portion of your portfolio to growth-oriented assets like stocks.

3. Time Horizon is Your Friend: Market fluctuations are inevitable. A long time horizon allows you to ride out downturns and benefit from long-term market growth. Don't panic sell during corrections.

Essential Investment Vehicles

Essential Investment Vehicles for Your 20s

1. Retirement Accounts (Tax-Advantaged): These should be your first priority.

2. Taxable Brokerage Accounts: Once you've maximized your retirement accounts, open a standard investment account.

3. High-Yield Savings Accounts (for Short-Term Goals): While not an "investment" in the traditional sense, a high-yield savings account is crucial for your emergency fund and short-term savings goals, offering better returns than traditional bank accounts.

What to look for

- 401(k) / 403(b) (Employer-Sponsored): If your employer offers a match, contribute at least enough to get the full match - it's free money! Contributions are pre-tax (traditional) or after-tax (Roth), reducing taxable income or allowing tax-free withdrawals in retirement.

- Roth IRA: An excellent option for young adults. Contributions are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. Your income in your 20s is likely lower, meaning you're in a lower tax bracket, making Roth contributions particularly advantageous.

- Traditional IRA: Contributions may be tax-deductible, and taxes are paid upon withdrawal in retirement.

- ETFs (Exchange-Traded Funds) & Index Funds: These are ideal for beginners. They offer broad diversification across hundreds or thousands of companies, are low-cost, and generally outperform actively managed funds over the long term. Focus on total market index funds (e.g., S&P 500 index) or target-date funds.

- Individual Stocks: While exciting, individual stock picking requires significant research and carries higher risk. For most in their 20s, a diversified fund approach is more prudent.

The Power of

The Power of Automation in Investing

Just as Sumyfi automates your financial tracking, automating your investments is key to consistency.

What to look for

- Automatic Contributions: Set up automatic transfers from your checking account to your investment accounts (401k, IRA, brokerage) on a regular schedule (e.g., payday).

- Dollar-Cost Averaging: This strategy involves investing a fixed amount of money at regular intervals, regardless of market fluctuations. It reduces the risk of investing a large sum at an unfavorable time and smooths out market volatility over time.

Diversification: Your Shield

Diversification: Your Shield Against Volatility

Never put all your eggs in one basket. Diversification means spreading your investments across different asset classes, industries, and geographies.

By embracing these investment principles, you're not just saving; you're actively growing your wealth and accelerating your ability to build net worth in your 20s.

What to look for

- Asset Allocation: Determine a suitable mix of stocks and bonds based on your age and risk tolerance. In your 20s, a higher allocation to stocks (e.g., 80-90%) is often appropriate.

- Global Exposure: Don't limit yourself to your home country's market. Invest in international funds to capture global growth.

Pillar 4: Asset

Pillar 4: Asset Accumulation Beyond Investments

While stocks and funds are primary drivers, other forms of assets can also contribute significantly to your net worth.

Real Estate: A

Real Estate: A Long-Term Net Worth Driver (Considerations for 20s)

For many, real estate represents a significant portion of their net worth. While buying a home in your early 20s might not be feasible for everyone, it's a goal worth planning for.

1. The "House Hacking" Strategy: Consider buying a multi-unit property and living in one unit while renting out the others. The rental income can cover a significant portion, or even all, of your mortgage, allowing you to build equity at a much faster pace.

2. Saving for a Down Payment: Even if you're not ready to buy now, start saving for a down payment in a high-yield savings account. The larger your down payment, the lower your mortgage and interest payments.

3. Understanding the Market: Educate yourself on local real estate markets, property taxes, and the costs associated with homeownership.

4. REITs (Real Estate Investment Trusts): If direct ownership isn't feasible, consider investing in REITs through your brokerage account. These allow you to invest in real estate portfolios without the complexities of direct property management.

Valuables & Intellectual

Valuables & Intellectual Property: Untapped Assets

While less liquid, certain assets can contribute to your net worth.

1. Collectibles & Art: If you have a passion for collecting, understand the market value of your items. Be cautious, as these can be speculative.

2. Intellectual Property: If you create original works (books, music, software, patents), your intellectual property can be a significant asset, generating royalties or licensing fees over time. Protect it legally.

Sumyfi allows you to manually add and track the estimated value of these less liquid assets, providing an even more holistic view of your total net worth.

Pillar 5: Protecting

Pillar 5: Protecting Your Financial Future (Risk Management)

Building net worth isn't just about accumulating assets; it's also about safeguarding them. A single unexpected event can derail years of progress.

Building an Emergency

Building an Emergency Fund: Your Financial Safety Net

This is non-negotiable. An emergency fund is 3-6 months' worth of essential living expenses (rent, food, utilities, transportation, insurance) stored in an easily accessible, liquid account, preferably a high-yield savings account.

What to look for

- Purpose: To cover unexpected job loss, medical emergencies, car repairs, or other unforeseen financial shocks without going into debt or having to sell investments at a loss.

- Priority: Build this *before* aggressively investing beyond your employer match.

Insurance Essentials: Safeguarding

Insurance Essentials: Safeguarding Your Assets and Income

Insurance acts as a financial shield against catastrophic losses.

1. Health Insurance: Critical in your 20s. A single medical emergency without coverage can lead to crippling debt.

2. Auto Insurance: Required by law in most places, protects you from financial liability in accidents.

3. Renter's/Homeowner's Insurance: Protects your belongings from theft, fire, and other perils. Essential even if you rent.

4. Disability Insurance: Often overlooked, this protects your most valuable asset: your ability to earn an income. If you become unable to work due to illness or injury, disability insurance provides a portion of your income. Consider it, especially if you have dependents or significant financial obligations.

5. Life Insurance: If you have dependents (e.g., a spouse, children) or co-signed loans, term life insurance is crucial to protect them financially in the event of your untimely death.

Estate Planning Basics

Estate Planning Basics (Even in Your 20s)

While it might seem premature, even basic estate planning is prudent.

What to look for

- Will: Designate who inherits your assets and, if applicable, who would be guardian to minor children.

- Power of Attorney: Appoint someone to make financial and medical decisions on your behalf if you become incapacitated.

- Beneficiary Designations: Ensure your retirement accounts and life insurance policies have up-to-date beneficiary designations, as these supersede your will.

The Sumyfi Advantage:

The Sumyfi Advantage: Accelerating Your Net Worth Journey

In an era where financial complexity often leads to paralysis, Sumyfi stands out as the ultimate modern solution for anyone serious about how to build net worth in your 20s. It's not just a tool; it's a strategic partner.

Real-time Financial Insights

Real-time Financial Insights

Gone are the days of waiting for monthly statements or manually updating spreadsheets. Sumyfi provides a live, dynamic view of your financial health. See your net worth fluctuate with market changes, track your spending as it happens, and understand your cash flow in real-time. This immediate feedback loop is invaluable for making timely, informed decisions.

Seamless Integration Across

Seamless Integration Across Thousands of Institutions (US & Canada)

Whether you bank with a major national institution or a local credit union, have investment accounts with various brokerages, or hold loans across different lenders, Sumyfi connects to virtually all of them. Our robust, agile engineering ensures secure and reliable data synchronization, giving you a truly comprehensive financial picture without missing a single piece of the puzzle. This broad compatibility is a game-changer for individuals with diverse financial portfolios.

The End of

The End of Manual Spreadsheets

Sumyfi's core mission is to liberate you from the tedious, error-prone world of manual financial tracking. Its automated transaction categorization, real-time net worth calculations, and intuitive budgeting tools eliminate the need for complex spreadsheets, freeing up your time and mental energy to focus on strategy rather than data entry. This streamlined approach fosters consistent engagement, which is critical for long-term financial success.

A Modern Alternative

A Modern Alternative to Legacy Apps

Many existing personal finance apps are either clunky, outdated, or lack the comprehensive feature set required for sophisticated wealth building. Sumyfi was built for the modern user, with a slick, crystal-clear interface that makes financial management not just easy, but enjoyable. It offers a superior, more integrated experience than many alternatives, providing a fresh perspective on your finances.

Are you tired of fragmented financial views and clunky interfaces?

[Discover why Sumyfi is the leading Mint Alternative and a superior choice for modern finance management.](https://www.sumyfi.com/mint-alternative)

For our Canadian users, Sumyfi offers unparalleled local integration and features.

[Explore why Sumyfi is the Best Budgeting App in Canada.](https://www.sumyfi.com/best-budgeting-app-canada)

Overcoming Psychological Barriers

Overcoming Psychological Barriers to Wealth Building

Building net worth isn't purely analytical; it's also deeply psychological. Your 20s present unique mental hurdles.

1. Impatience: The desire for instant gratification can be strong. Remember that wealth building is a marathon, not a sprint. Celebrate small victories and trust the process.

2. Fear of Missing Out (FOMO): Seeing peers spend on experiences or luxury items can create pressure. Stay focused on your long-term goals and remember the power of delayed gratification. Your future self will thank you.

3. Financial Literacy Gaps: Many young adults feel overwhelmed by financial jargon. Commit to continuous learning. Read books, listen to podcasts, and leverage tools like Sumyfi that simplify complex data.

4. Comparison Trap: Avoid comparing your financial journey to others. Everyone's circumstances are different. Focus on your own progress and celebrate your milestones.

5. The Starting Point Myth: Don't let a negative net worth or a modest income discourage you. Everyone starts somewhere. What matters is the direction you're heading and the consistency of your efforts.

Discipline, consistency, and a long-term perspective are your most powerful allies in this journey.

Your Action Plan:

Your Action Plan: How to Build Net Worth in Your 20s, Starting Today

Here's a distilled, actionable plan to kickstart your net worth journey:

1. Get Your Financial Baseline:

2. Master Your Spending:

3. Prioritize Debt Reduction:

4. Build Your Safety Net:

5. Start Investing (Now!):

6. Boost Your Income:

7. Educate Yourself Continuously:

8. Regularly Review and Adjust:

What to look for

- Sign up for Sumyfi: Connect all your accounts and get an instant, accurate picture of your current net worth. This is your starting point.

- Review Your Cash Flow: Use Sumyfi to understand exactly where your money is coming from and where it's going.

- Create a Budget: Implement a budget (50/30/20, zero-based, or value-based) using Sumyfi's automated tools.

- Identify & Cut Unnecessary Expenses: Use Sumyfi's transaction insights to find areas to reduce spending, especially recurring subscriptions.

- List All Debts: Use Sumyfi to see all your liabilities clearly.

- Attack High-Interest Debt: Develop a plan to aggressively pay down credit card debt and high-interest personal loans.

- Establish an Emergency Fund: Start saving 3-6 months of living expenses in a high-yield savings account. Automate transfers.

- Maximize Employer Match: If offered, contribute enough to your 401(k) to get the full company match.

- Open a Roth IRA: Set up automatic contributions, even if small, and invest in broad market index funds or ETFs.

- Automate All Investments: Set it and forget it.

- Assess Your Skills: Identify areas for professional development.

- Explore Side Hustles: Find ways to bring in extra income that aligns with your skills and interests.

- Read financial books, follow reputable financial news, and stay informed.

- Use Sumyfi

FAQs

Frequently asked questions about how to build net worth in your 20s

Is Sumyfi really a strong option for how to build net worth in your 20s?

Yes, especially if the real goal behind the search is reducing fragmentation. Sumyfi is strongest for users who want connected accounts, clear budgeting, visible goals, recurring-spend awareness, and modern AI-assisted explanations in one place rather than separate disconnected tools.

What matters most when comparing options for how to build net worth in your 20s?

Account connectivity, spending clarity, recurring-charge visibility, budgeting depth, goal support, trust posture, and ease of repeat use matter most. Those factors influence whether the tool becomes part of your real routine or remains a short-lived experiment.

How does Sumyfi help people researching how to build net worth in your 20s day to day?

Sumyfi helps by keeping the wider money picture visible for people trying to build wealth early with better account visibility and spending control. That makes it easier to understand tradeoffs, track progress, and act on recurring patterns without rebuilding the context in separate tools.

What makes a finance app easier to keep using over time?

Low-friction review loops matter most. If the dashboard helps you connect accounts, understand patterns quickly, and take the next action without extensive manual cleanup, you are much more likely to stay engaged. That ongoing usability matters more than a long feature list.

Who is How to Build Net Worth in Your 20s usually best for?

It is usually best for people in their 20s who want clearer financial visibility without building a heavy manual system. Sumyfi is strongest when the user wants practical weekly clarity more than niche complexity for its own sake.

Supporting articles

Read related explainers before you commit

These blog articles add broader context around budgeting habits, expense tracking, automation, and product-fit questions so readers can keep digging into the same decision from a few useful angles.

Blog explainer

Best Budgeting App in 2026

A good bridge for users whose net-worth tracking still depends on day-to-day budgeting habits.

Read article

Blog explainer

Automate Your Budget with Sumyfi

Useful when long-term progress depends on a cleaner weekly system underneath it.

Read article

Blog explainer

Best Budget App in Canada

Useful for Canadian net-worth and dashboard searches that need local context.

Read article

Keep exploring

Continue the same decision journey

These related guides keep the search useful for both visitors and search engines by routing buyers into the next relevant comparison, budgeting, dashboard, or net-worth question.

Related guide

How to Switch from Mint

moving from Mint to a cleaner financial tracking system for accounts, subscriptions, savings goals, and weekly money review

Read How to Switch from Mint

Related guide

Connect All Bank Accounts in One App

bringing checking, savings, credit cards, and investment accounts into one unified dashboard

Read Connect All Bank Accounts in One App

Related guide

Best Subscription Tracker App

finding recurring charges, monitoring bills, and reducing waste from forgotten subscriptions

Read Best Subscription Tracker App

Related guide

Best Savings Tracking Software

tracking savings goals, progress, and recurring contributions inside a broader financial dashboard

Read Best Savings Tracking Software

Related guide

Best Net Worth Tracker Canada

tracking assets, liabilities, savings, and investing progress for Canadians

Read Best Net Worth Tracker Canada

Related guide

Best Net Worth Tracker USA

tracking net worth, debt, and account balances across American financial institutions

Read Best Net Worth Tracker USA

Topic cluster

Keep exploring the same decision journey

More net worth search pages

Explore adjacent pages in the same topic so the search journey stays focused instead of jumping between unrelated finance queries.

Net Worth Search

Best Net Worth Tracker Canada

tracking assets, liabilities, savings, and investing progress for Canadians

Net Worth Search

Best Net Worth Tracker USA

tracking net worth, debt, and account balances across American financial institutions

Net Worth Search

Best Net Worth Dashboard App

watching net worth move over time with a dashboard that also reflects daily spending decisions

Net Worth Search

How to Track Net Worth Easily

tracking assets and debt without creating a complicated personal spreadsheet system

Related use cases and adjacent searches

Branch into nearby searches that tend to appear in the same decision journey, from alternatives to dashboards to budgeting help.

Net Worth Search

Free Net Worth Tracking App

starting net worth tracking with a clean dashboard and low setup friction

Net Worth Search

Best Wealth Tracking App

tracking assets, liabilities, and progress toward long-term financial independence

Net Worth Search

Personal Asset Tracker App

tracking financial accounts and personal assets inside one overview

Net Worth Search

Debt + Net Worth Tracker

seeing debt reduction and net worth growth together instead of in separate tools

Guide hub

Browse the full Sumyfi topic cluster

Move from one question to the next through budgeting, dashboard, subscription, AI, and comparison guides that support the same decision journey.