The Best Budgeting App in Canada (2026)

The best budgeting app in Canada should not just categorize spending. It should help Canadians review accounts, recurring bills, goals, and monthly drift in one workflow that still feels easy to use after the first month.

Built around Canadian budgeting intent instead of a generic North American template.

Centers recurring expenses, cash-flow visibility, and realistic weekly budgeting.

Designed for a budgeting habit Canadians can actually keep using.

What matters most

The best budgeting app in Canada should make weekly money reviews feel simpler.

This search usually comes from someone who already knows their current setup is too fragmented. They may be checking bank apps, a spreadsheet, and a mental list of bills, yet still not feeling in control of what the month really looks like. The better budgeting app should close that gap quickly.

For Canadian users, that means more than a polished budgeting interface. The product needs to feel grounded in recurring bills, account-connected visibility, and a review flow that can survive normal life pressure without becoming another spreadsheet chore.

If you want a Canadian budgeting app that helps you review spending, recurring bills, and goals inside one clearer workflow, Sumyfi is the stronger fit.

At a glance

What this comparison covers

Table of contents

Jump to the part you actually care about

What to compare first

Three things to decide before you pick a tool

If you want a Canadian budgeting app that helps you review spending, recurring bills, and goals inside one clearer workflow, Sumyfi is the stronger fit.

Best for people in Canada who want finding a budgeting app that works well with Canadian bank accounts, recurring bills, and everyday planning.

Canada context changes what counts as a believable, useful finance workflow.

Buyer checklist

What Canadian budgeting shoppers should verify before they commit

- Does the app feel relevant to Canadian household budgeting instead of like a repackaged U.S. workflow?

- Can you connect the budget to real account movement and recurring bills without extra spreadsheet cleanup?

- Will the review still feel manageable during a busy month with groceries, rent, and surprise expenses?

- Does the product help you act on drift quickly instead of only showing you the drift after the fact?

- Is the company credible enough to trust for an ongoing budgeting routine?

Why Sumyfi

Built for Canadian households that want clarity without a heavy maintenance burden

The strongest case for Sumyfi here is that it turns budgeting into a connected weekly review instead of a separate financial chore. Canadians can connect visibility, recurring spending, and goal progress inside one environment.

Comparison table

Best budgeting apps in Canada compared

This comparison is intentionally practical. It focuses on Canadian fit, budgeting usefulness, and whether the app keeps recurring bills, goals, and the full account picture connected enough to support real monthly decisions.

| Decision area | Sumyfi | YNAB | Monarch Money | Rocket Money | Copilot Money |

|---|---|---|---|---|---|

| Canadian fit | Strong Canada + U.S. positioning | Usable, but not Canada-led | Available, but not built around Canada first | More U.S.-centered | Less Canada-specific positioning |

| Budgeting style | Integrated with the full dashboard | Methodology-heavy budgeting first | Flexible premium budgeting | Lighter budgeting, broader spend control | Clean modern money overview with budgeting support |

| Automatic syncing | Yes | Partial depending on workflow | Yes | Yes | Yes |

| Subscription tracking | Built into wider dashboard | Secondary | Available | Core strength | Secondary |

| Goal tracking | Yes | Strong budgeting-centric goal planning | Yes | More limited emphasis | Moderate |

| Net worth tracking | Yes, tied to the full account picture | Less central | Yes | More limited | Yes |

| Ease of repeat use | Built for a broad weekly review habit | Best for users who want tighter structure | Good for premium-dashboard users | Good for expense and subscription review | Good for users prioritizing a polished overview |

| Pricing | Check live pricing | Paid subscription | Paid subscription | Freemium + paid tiers | Paid subscription |

| Free trial | Check current offer | Typically yes | Typically yes | Typically yes | Typically yes |

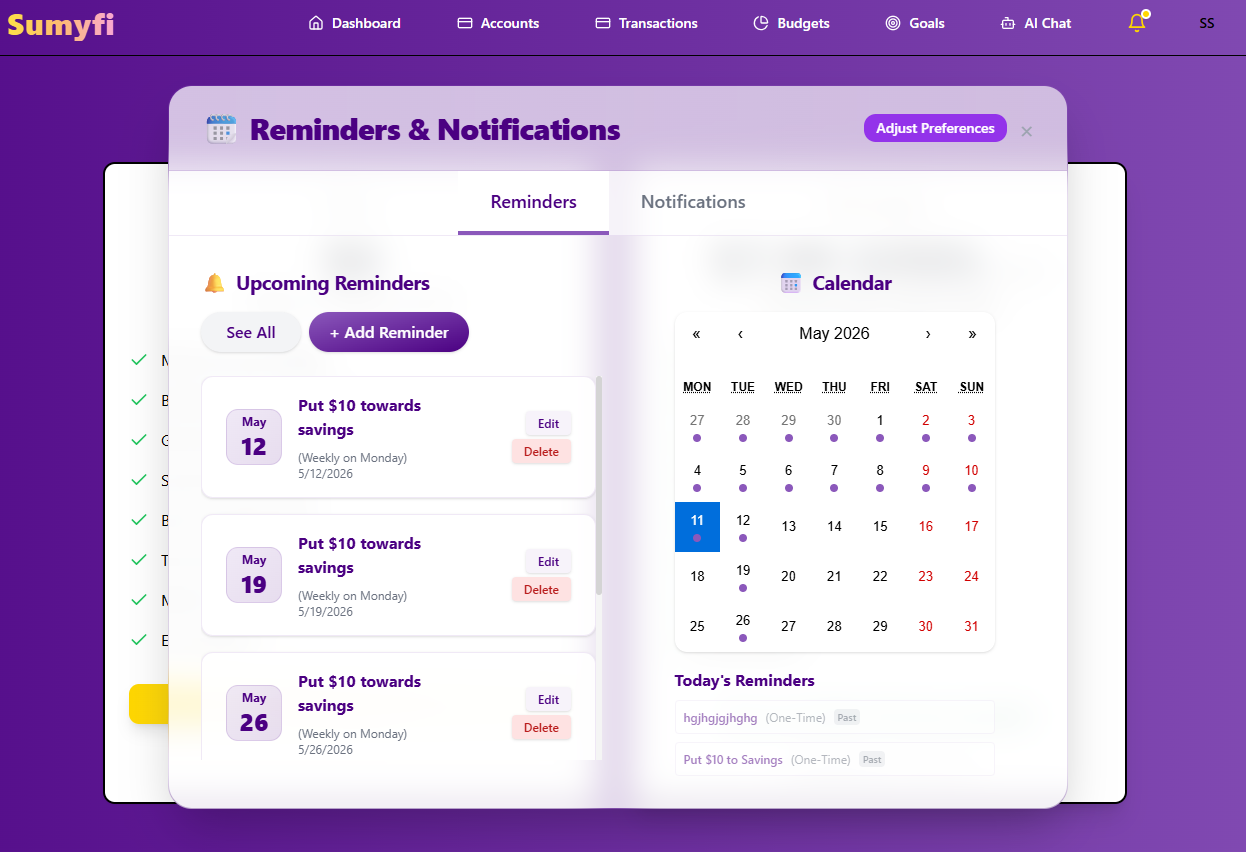

Product screenshots

See how budgeting fits into the wider Sumyfi workflow

A Canadian budgeting guide should show more than category charts. These product surfaces show how budgets, accounts, goals, and recurring bills live together in one modern dashboard.

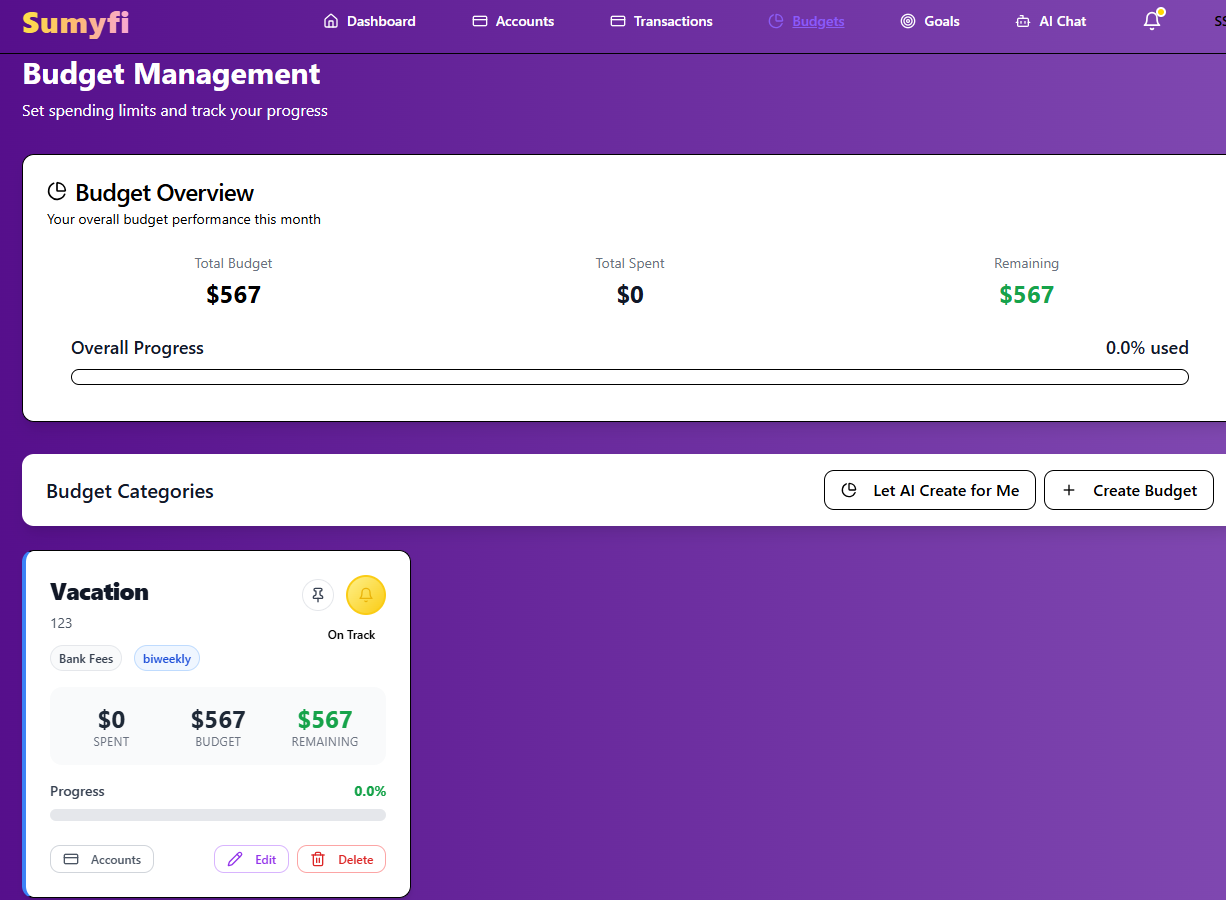

Budgets

Budgets that stay connected to live financial context instead of becoming a separate monthly exercise.

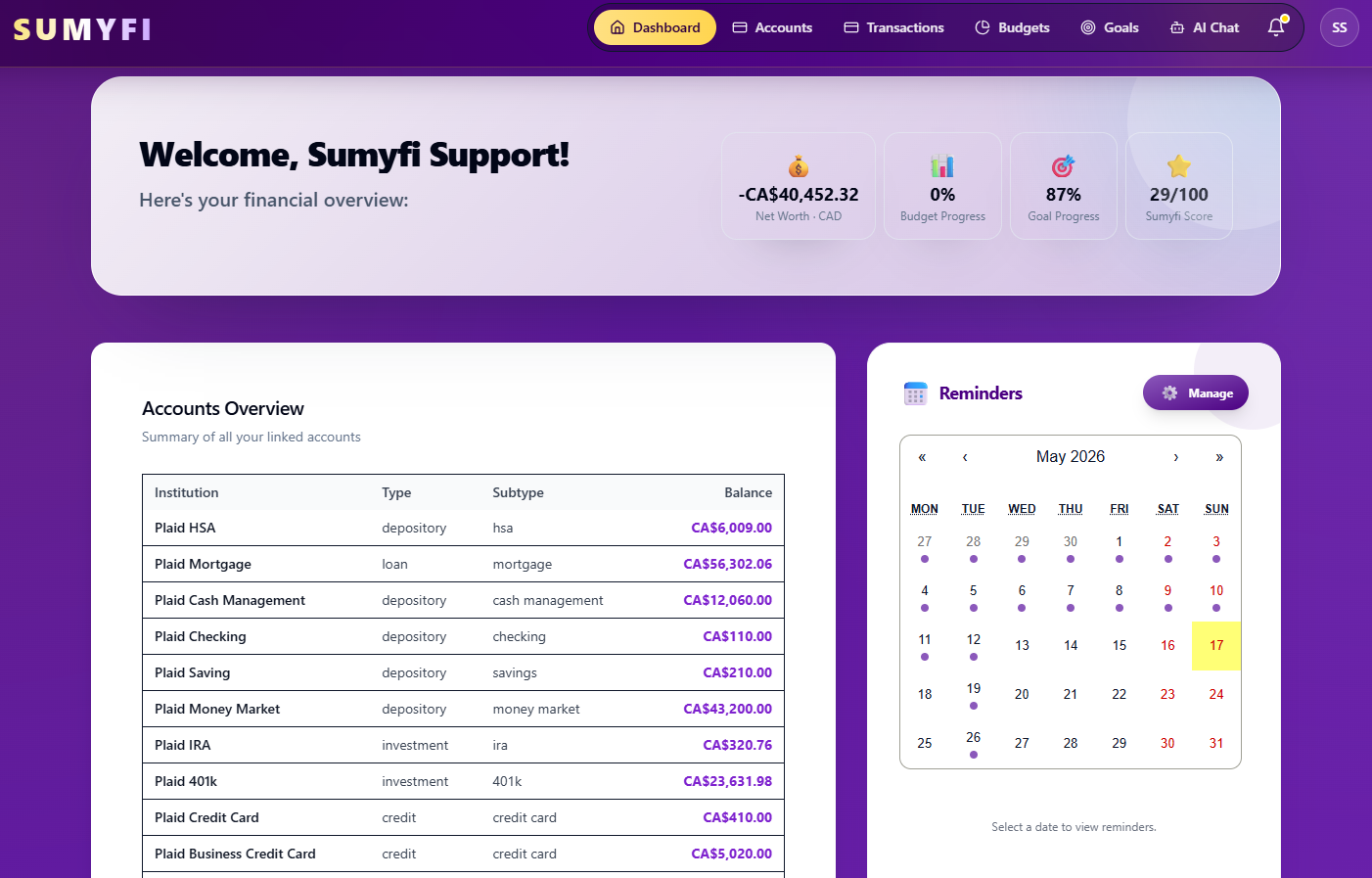

Dashboard

A top-level dashboard that keeps the budget attached to the broader account picture.

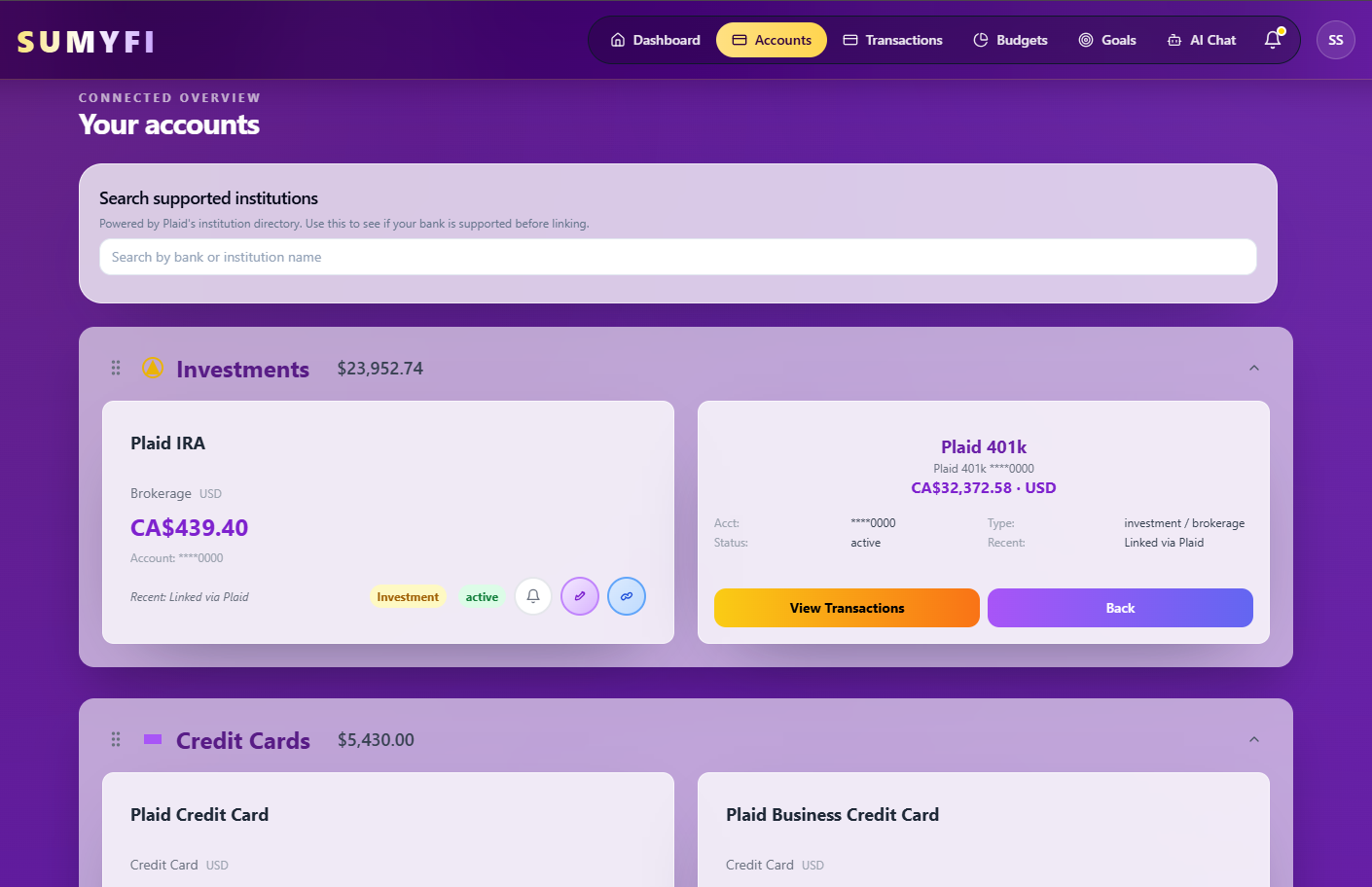

Accounts

Accounts and balances remain visible beside the planning layer, which makes the budget easier to trust.

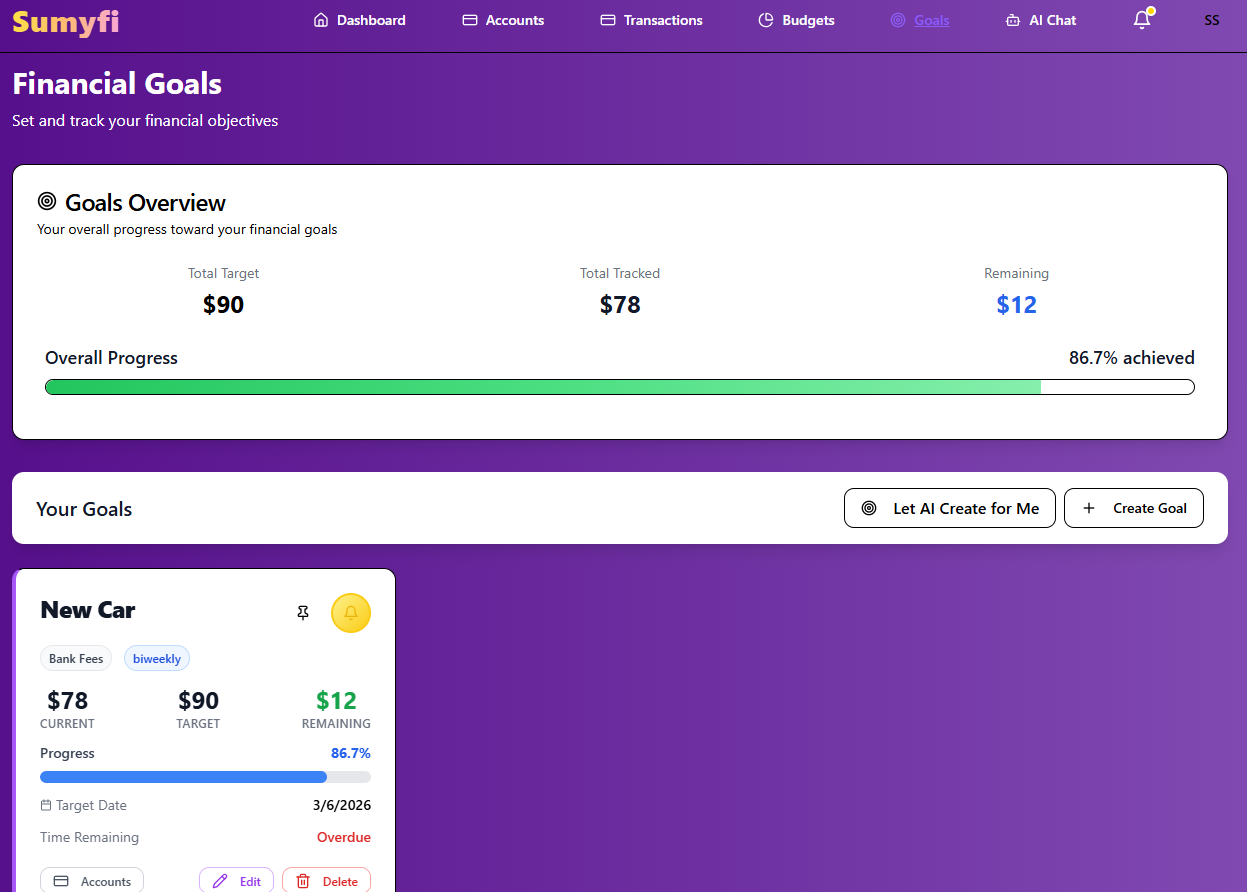

Goals

Goals stay connected to the same spending and budget signals that affect progress.

Subscriptions

Recurring bills and subscriptions stay visible so they can be budgeted against realistically.

Trust surfaces

Trust matters more than surface-level marketing in finance

In a YMYL category, buyers need visible support, security, coverage, and public accountability before they are comfortable connecting money data or acting on product guidance.

Security and privacy

Serious buyers need visible security, privacy, and data-handling pages before they trust a finance product.

Support and help center

A visible help center gives cautious buyers a clearer path before signup.

Institution coverage

Institution coverage matters because connected-account trust is part of the product story for dashboard and aggregation buyers.

Public launch signal

External product-discovery pages add another public trust surface beyond the marketing site itself.

Public roadmap on GitHub

A public roadmap repo gives buyers and readers another transparent trust surface around product direction and external mentions.

Proof block

Signals Canadian budgeting shoppers look for before signing up

Canadian budgeting context

Automatic syncing

Recurring bills

"I want a budget I can maintain in Canada without feeling like I need a spreadsheet backup plan."

"If the account picture and the budget live too far apart, I already know I am going to stop checking it."

Why budgeting apps disappoint

Most budgeting apps in Canada fail when the budget gets separated from the real account picture

A lot of budgeting apps sound good in theory because they promise more discipline, better categories, or a clearer monthly plan. In practice, many Canadians abandon them because the app starts feeling like one more system to maintain on top of actual bank accounts, recurring bills, and everyday financial surprises. The more the budget lives apart from the live account picture, the more mental reconciliation the user has to do every week.

That problem is often underexplained in Canadian search results. Many roundup pages treat every budgeting app as if the only difference is the feature checklist. But the real question is whether the product helps a Canadian household make faster, better decisions during a normal month with rent, groceries, subscriptions, debt payments, and savings goals all competing for attention.

The best budgeting app in Canada therefore is usually the one that keeps the budget connected to accounts, recurring expenses, and progress tracking instead of turning budgeting into a separate chore. When the app reduces interpretation work, people keep using it longer.

What to look for

- The budget has to stay close to the account picture

- Canadian users need an app that feels locally believable, not just globally available

- Repeat use matters more than feature count

What to look for

What actually matters when Canadians compare budgeting apps

Start with Canadian fit and automatic syncing. If the app feels disconnected from Canadian financial life or depends on too much manual upkeep, retention usually collapses fast. Buyers should also look at whether subscriptions and recurring bills stay visible, because recurring pressure is often what makes or breaks a monthly budget in real life.

Next, evaluate how the product handles planning depth. Some apps are strong at methodology, some are strong at recurring-expense visibility, and some are stronger at giving the user one broader dashboard for accounts, budgets, goals, and net worth. The winner depends on whether the household wants a narrow budgeting system or a full financial operating view.

The strongest apps also feel modern and forgiving. A useful budgeting product should make it faster to spot drift, connect spending to goals, and understand where pressure is building, without making the user feel like every month requires a financial reset project.

What to look for

- Canadian support and credible cross-account syncing

- Budgeting connected to recurring bills and subscriptions

- Goal tracking and net worth visibility in the same product

- A modern interface that encourages repeat use

- Enough simplicity for everyday households, not only power users

Why Sumyfi stands out

Why Sumyfi is a compelling budgeting choice for Canadians in 2026

Sumyfi is strongest when the buyer wants budgeting to live inside a broader money system instead of a rigid budgeting silo. The app is designed to keep connected accounts, subscriptions, goals, budgets, and net worth close enough together that the budget actually helps with the next decision instead of just documenting the last one.

That makes the product a strong fit for Canadian households who do not want to choose between budgeting and visibility. Rather than forcing the user into a budgeting-only frame, Sumyfi aims to make the budget one part of a larger dashboard they can rely on every week. That usually creates better sticking power than tools that feel methodologically strong but practically disconnected.

The interface also matters. Many finance apps feel visually dated or too dense, which raises the friction of checking them. Sumyfi benefits from a more premium and current product surface, which supports the kind of regular use budgeting tools need if they are going to be effective beyond the first month.

What to look for

- Budgets, accounts, subscriptions, goals, and net worth kept together

- Built for Canadian users who want clarity without spreadsheet upkeep

- A cleaner weekly-review workflow than narrow budgeting-only tools

- Modern dashboard feel that supports better long-term retention

What other apps miss

Where competing budgeting apps often create friction for Canadians

Some apps are excellent if you want a deeply structured budgeting method and do not mind maintaining it closely. Others are better for subscription visibility or broad premium-style overviews. But many Canadians are not looking for a budgeting hobby. They want one product that helps them understand the month quickly and stay oriented without juggling extra tools.

That is where the category gets tricky. The more the product splits budgeting, recurring bills, and account visibility into separate surfaces or mental models, the less likely the user is to keep coming back. Poor Canadian support makes that even worse because the whole workflow starts to feel imported instead of grounded in the user's real financial life.

The better budgeting page should be honest about that tradeoff. Methodology depth, premium polish, and subscription tools all matter, but the strongest everyday budgeting app is the one that reduces friction across the whole household money loop.

What to look for

- Rigid systems can create more maintenance than normal households can sustain

- Subscription-first apps often underserve broader budgeting needs

- Premium dashboards can still feel incomplete if planning and recurring pressure stay too disconnected

Month-two test

How to tell whether best budgeting app canada will still feel usable once real life hits

A budgeting app should be judged after the initial motivation spike, not during it. The real question is whether the system still feels manageable once real spending variance, recurring bills, and an imperfect week show up. If the tool only feels good under ideal conditions, it is probably too brittle to become a habit.

The better product helps users stay oriented around finding a budgeting app that works well with Canadian bank accounts, recurring bills, and everyday planning even when the month becomes messy. That means clearer recurring-spend visibility, easier adjustments, and enough dashboard context that the budget still feels tied to reality instead of becoming a separate ritual.

What to look for

- Should stay usable during irregular weeks

- Should make recurring pressure easier to spot

- Should help the next decision, not only document the last one

Weekly review

The budget should make the next adjustment easier, not add more homework

Most budgeting systems fail through invisible friction. The user spends too much time reconciling categories, remembering recurring costs, or translating raw account movement into a meaningful plan. The better product removes enough of that hidden work that the review loop starts to feel sustainable.

When the system lowers mental overhead, users are more likely to keep checking the app, notice drift earlier, and make smaller course corrections before problems compound. That is the practical standard that matters more than any theoretical budgeting philosophy.

Canada buying context

Why Canada buyers often judge this category a little differently

Canada buyers usually care about more than whether the product can technically be used in their market. They want the workflow to feel locally believable, the account and planning assumptions to feel familiar enough, and the whole review experience to map to how they actually think about money week to week.

That regional fit matters because the better product for finding a budgeting app that works well with Canadian bank accounts, recurring bills, and everyday planning should feel credible before the user is fully invested in setup. A dashboard that feels imported or generic can lose trust quickly even when its surface features look good on paper.

What matters after week one

How to tell whether the workflow will still help after week one

The best test is still a real weekly workflow. If the product makes balances, recurring activity, and next actions easier to review without a lot of cleanup, it is probably a good fit. If it still leaves you stitching the story together manually, the problem is not solved yet.

Sumyfi is strongest when the dashboard, planning layer, and recurring money decisions stay connected. That makes it easier to decide whether the product genuinely improves how you handle finding a budgeting app that works well with Canadian bank accounts, recurring bills, and everyday planning.

Why people hesitate

The biggest buying risk is usually choosing a tool that looks clearer than it feels

Finance buyers often know the category language well enough to compare features, but still struggle to picture what the product will feel like in ordinary use. That uncertainty is rational. A lot of apps sound complete during research and still create too much hidden work once the user tries to rely on them weekly.

The better explanation lowers that uncertainty by showing how the workflow behaves under normal life pressure. That is usually more persuasive than adding another layer of generic claims.

Decision speed

What makes a tool easier to act on quickly

People search these categories because they want relief from uncertainty, drift, or unnecessary effort. The product that wins is usually the one that makes the next decision easier once the user opens it. If the app still requires a lot of interpretation or a second system to translate the data, its value plateaus quickly.

That is why connected design matters. When visibility, recurring patterns, and planning context stay close together, the app becomes easier to trust and easier to keep using.

FAQs

Frequently asked questions about best budgeting app canada

Is Sumyfi really a strong option for best budgeting app canada?

Yes, especially if the real goal behind the search is reducing fragmentation. Sumyfi is strongest for users who want connected accounts, clear budgeting, visible goals, recurring-spend awareness, and modern AI-assisted explanations in one place rather than separate disconnected tools.

What matters most when comparing options for best budgeting app canada?

Account connectivity, spending clarity, recurring-charge visibility, budgeting depth, goal support, trust posture, and ease of repeat use matter most. Those factors influence whether the tool becomes part of your real routine or remains a short-lived experiment.

How does Sumyfi help people researching best budgeting app canada day to day?

Sumyfi helps by keeping the wider money picture visible for people trying to find a budgeting app that works well with Canadian bank accounts, recurring bills, and everyday planning. That makes it easier to understand tradeoffs, track progress, and act on recurring patterns without rebuilding the context in separate tools.

What makes a finance app easier to keep using over time?

Low-friction review loops matter most. If the dashboard helps you connect accounts, understand patterns quickly, and take the next action without extensive manual cleanup, you are much more likely to stay engaged. That ongoing usability matters more than a long feature list.

Who is Best Budgeting App Canada usually best for?

It is usually best for people in Canada who want clearer financial visibility without building a heavy manual system. Sumyfi is strongest when the user wants practical weekly clarity more than niche complexity for its own sake.

Does Canada context change what matters here?

Yes. Canada users usually care whether the product feels believable for their real banking and budgeting routine, not just whether the app looks polished in a generic comparison.

What is the best budgeting app in Canada?

The best budgeting app in Canada is the one that combines Canadian relevance, connected-account visibility, recurring-bill awareness, and a workflow you will still want to use after the first month. Sumyfi is built to compete on that broader combination rather than only one narrow budgeting method.

Do budgeting apps in Canada need to support automatic bank syncing?

For most people, yes. Automatic syncing matters because the budget becomes much harder to maintain when it drifts too far from real balances, recurring charges, and current transaction activity.

Is YNAB or Sumyfi better for Canadians?

YNAB is strong for users who want a more structured budgeting methodology. Sumyfi is stronger for Canadians who want a broader dashboard that keeps budgeting, subscriptions, accounts, goals, and net worth connected in one workflow.

Should Canadians choose a budgeting app or a full financial dashboard?

That depends on whether the real need is budgeting structure alone or a wider household money system. Many Canadians benefit more from a full dashboard because subscriptions, accounts, goals, and net worth all influence whether the budget is working.

Why do Canadians abandon budgeting apps so quickly?

Usually because the app creates too much maintenance, too much manual cleanup, or too much separation between the budget and the real account picture. The strongest budgeting apps lower friction instead of formalizing it.

Supporting articles

Read related explainers before you commit

These blog articles add broader context around budgeting habits, expense tracking, automation, and product-fit questions so readers can keep digging into the same decision from a few useful angles.

Blog explainer

Best Budget App in Canada

A Canada-specific explainer for bank fit, CAD handling, and post-Mint budgeting workflows.

Read article

Blog explainer

Best Budgeting App in 2026

A broader buyer guide for choosing a budgeting workflow that actually sticks.

Read article

Blog explainer

Zero-Based Budgeting Guide

Useful for stricter planning searches and category-control buyers.

Read article

Keep exploring

Next guides for Canadian budgeting buyers

The strongest budgeting guide should help the visitor move into the next relevant question, whether that is subscriptions, Mint alternatives, goals, or reducing spreadsheet dependence.

Related guide

Best Mint Alternative Canada

For Canadians comparing budgeting tools through the lens of post-Mint replacement research.

Read the Mint alternative guide

Related guide

Best Subscription Tracker App

For users whose budget problems are being driven primarily by recurring charges and subscription drift.

Compare subscription-tracking options

Related guide

Financial Goals App

For visitors who want budgeting to connect directly to savings targets and progress tracking.

See goal-tracking options

Related guide

How to Manage Money Without Spreadsheets

For users who are specifically trying to replace fragile spreadsheet budgeting with a more sustainable workflow.

See the spreadsheet-free path

Related guide

Why Most Budgeting Apps Fail After 30 Days

For readers who want to understand the behavior and retention problem behind weak budgeting tools.

Read why budgeting tools fail

Related guide

Best Net Worth Tracker Canada

For Canadians who want their budget connected to broader long-term progress instead of isolated monthly categories.

Explore Canadian net worth tracking

Topic cluster

Keep exploring the same decision journey

More budgeting search pages

Explore adjacent pages in the same topic so the search journey stays focused instead of jumping between unrelated finance queries.

Budgeting Search

Best Budgeting App USA

finding a budgeting app for American households that want spending visibility and account sync

Budgeting Search

Best Savings Tracking Software

tracking savings goals, progress, and recurring contributions inside a broader financial dashboard

Budgeting Search

Best Money App for Young Adults

giving young adults a simple money app for budgeting, subscriptions, and financial habits

Budgeting Search

Best Budgeting App for Young Adults

helping young adults budget without needing an advanced finance background

Canada money guides nearby

See other pages built around the same regional money context so visitors can keep exploring locally relevant workflows.

Subscription Search

Subscription Tracker Canada

tracking Canadian subscriptions, monthly bills, and recurring entertainment or app charges

Budgeting Search

Best Budgeting App Canada Reddit

the budgeting app Canadians compare when they want a practical recommendation, not just a generic list

Account Aggregation Search

Best Finance App Canada

finding one finance app for Canadian budgeting, account aggregation, and goal tracking

Budgeting Search

Best App for Canadians to Budget

helping Canadians budget with connected accounts and a clear dashboard

Guide hub

Browse the full Sumyfi topic cluster

Move from one question to the next through budgeting, dashboard, subscription, AI, and comparison guides that support the same decision journey.