Sumyfi vs Mint

Sumyfi vs Mint is less about nostalgia and more about whether former Mint users want a stronger post-Mint operating system for budgeting, recurring bills, and weekly money review.

Former Mint users are usually trying to replace a habit loop, not just compare feature lists.

The strongest product is the one that restores orientation and stays useful after the switch.

A Mint comparison can get stuck on nostalgia instead of whether the new system is actually better.

Legacy comparison context

The product should help former Mint users choose the better next system, not just relive the old one.

Mint still anchors how many shoppers think about personal finance software, but the more useful comparison is not Sumyfi versus Mint as if both were equally current options. It is whether the post-Mint buyer wants to rebuild the same habit loop on a stronger foundation.

That means The product should compare broader workflow quality, recurring-spend review, and whether the product gives former Mint users a cleaner weekly operating system than the one they lost.

If you want the better post-Mint workflow rather than the closest legacy reference point, Sumyfi is the stronger choice here.

At a glance

What this comparison covers

Table of contents

Jump to the part you actually care about

What to compare first

Three things to decide before you pick a tool

If you want the better post-Mint workflow rather than the closest legacy reference point, Sumyfi is the stronger choice here.

Best for everyday personal finance users who want comparing Sumyfi against the legacy standard many former Mint users still reference.

Use it like a fair workflow comparison with Mint, not a shallow feature table.

Buyer checklist

What former Mint users should compare first

- Are you looking for the most familiar interface or the strongest long-term weekly money system?

- Does the product connect budgets, subscriptions, goals, and account review in one place?

- Will the app still feel useful after the migration is complete?

- Does the replacement improve on Mint's old habit loop instead of only imitating it?

Why Sumyfi

Why Sumyfi is the stronger modern answer to former Mint expectations

Sumyfi works well for this need because the product is not trying to win by resemblance alone. It is better positioned to rebuild the weekly money habit around a fuller, more current workflow for spending, recurring bills, goals, and account visibility.

Comparison table

Sumyfi vs Mint

Exact pricing and plans can shift over time, so the most useful comparison is whether the product helps users move from fragmented financial data to clearer decisions with less maintenance.

| Decision area | Sumyfi | Mint |

|---|---|---|

| Primary workflow | One place for accounts, budgets, goals, recurring money decisions, and AI-supported explanations for people researching sumyfi vs mint. | Often built around a narrower workflow tied more specifically to the main use case behind this search. |

| Account visibility | Designed to keep everyday spending and the bigger financial picture visible together instead of splitting them into separate tools. | May emphasize one slice of the money picture more than the full system. |

| Ease of ongoing use | Built to reduce maintenance so the dashboard is easier to keep using week after week. | Can be useful, but may require more manual review, heavier setup, or a more specialized workflow. |

| Planning support | Supports budgeting, goal tracking, forward-looking decisions, and a cleaner review process in one experience. | Planning support varies depending on the product and the subscription tier you choose. |

| Trust surface | Public support, security, privacy, and AI usage pages help lower risk for serious shoppers before signup. | Trust signals depend on the company, and not every buyer gets the same level of clarity upfront. |

| Best fit | Best for people who want to compare Sumyfi against the legacy standard many former Mint users still reference without juggling separate tools and disconnected reviews. | Best for users who already know they want a narrower product centered on sumyfi vs mint. |

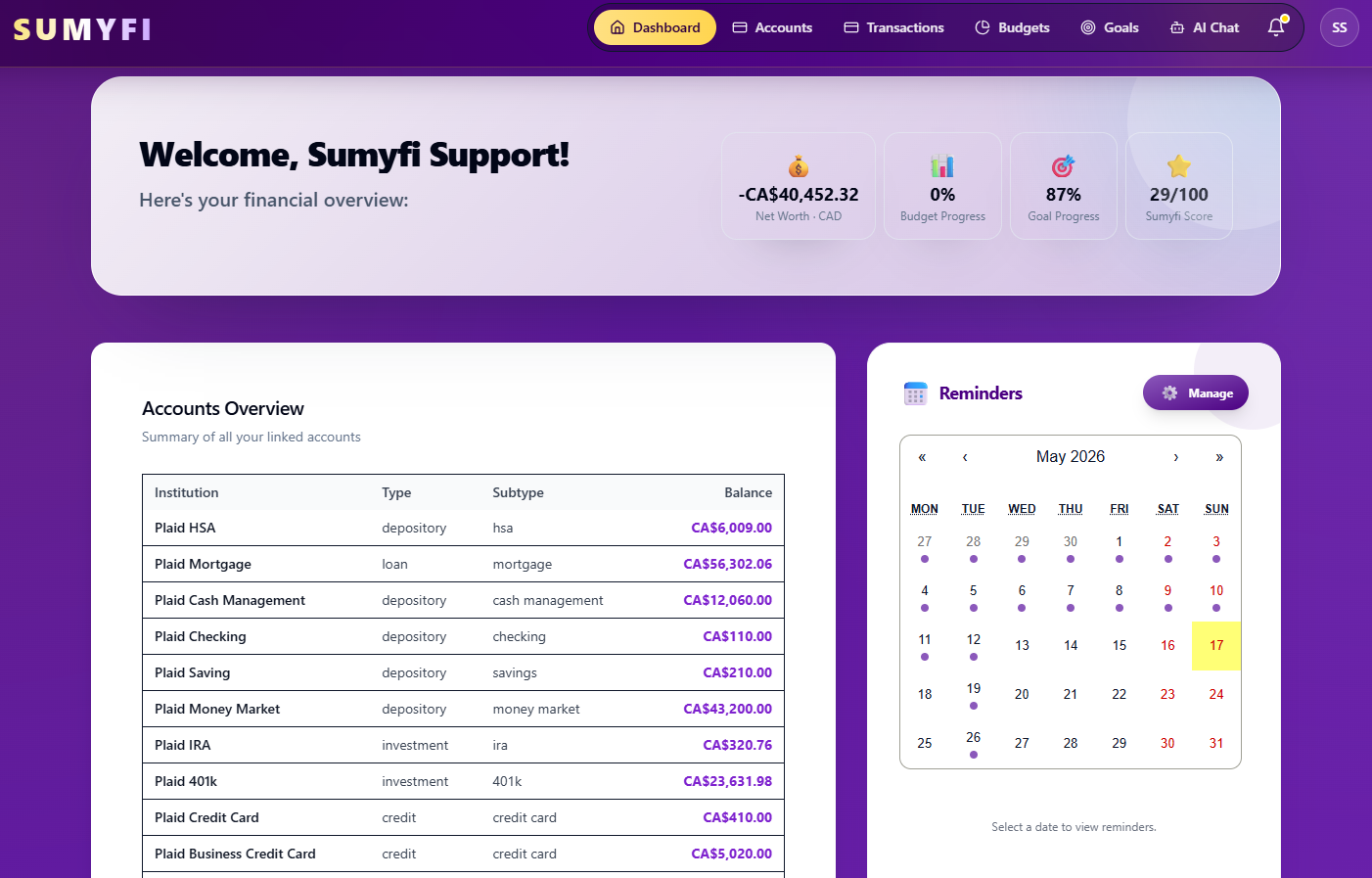

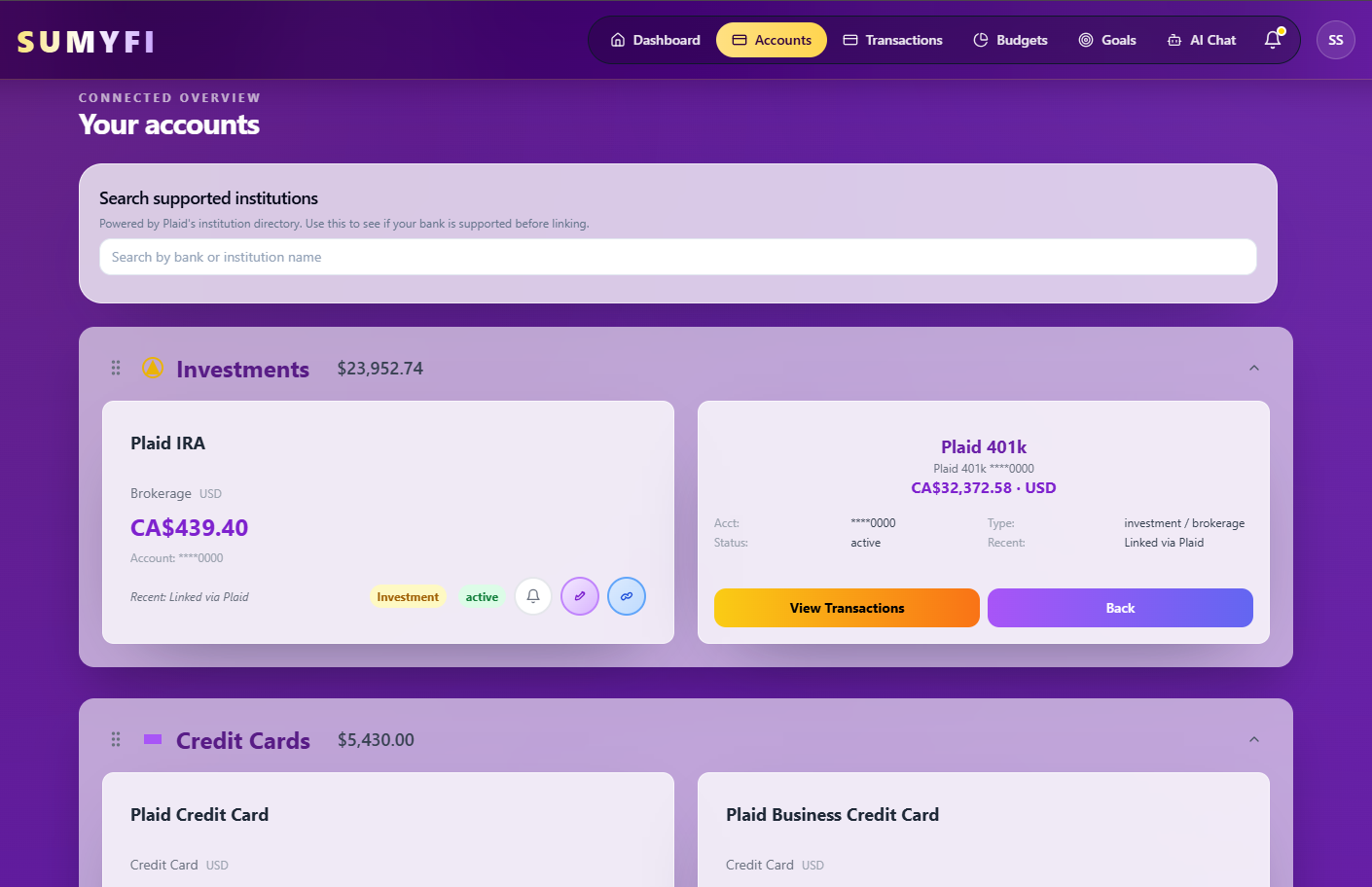

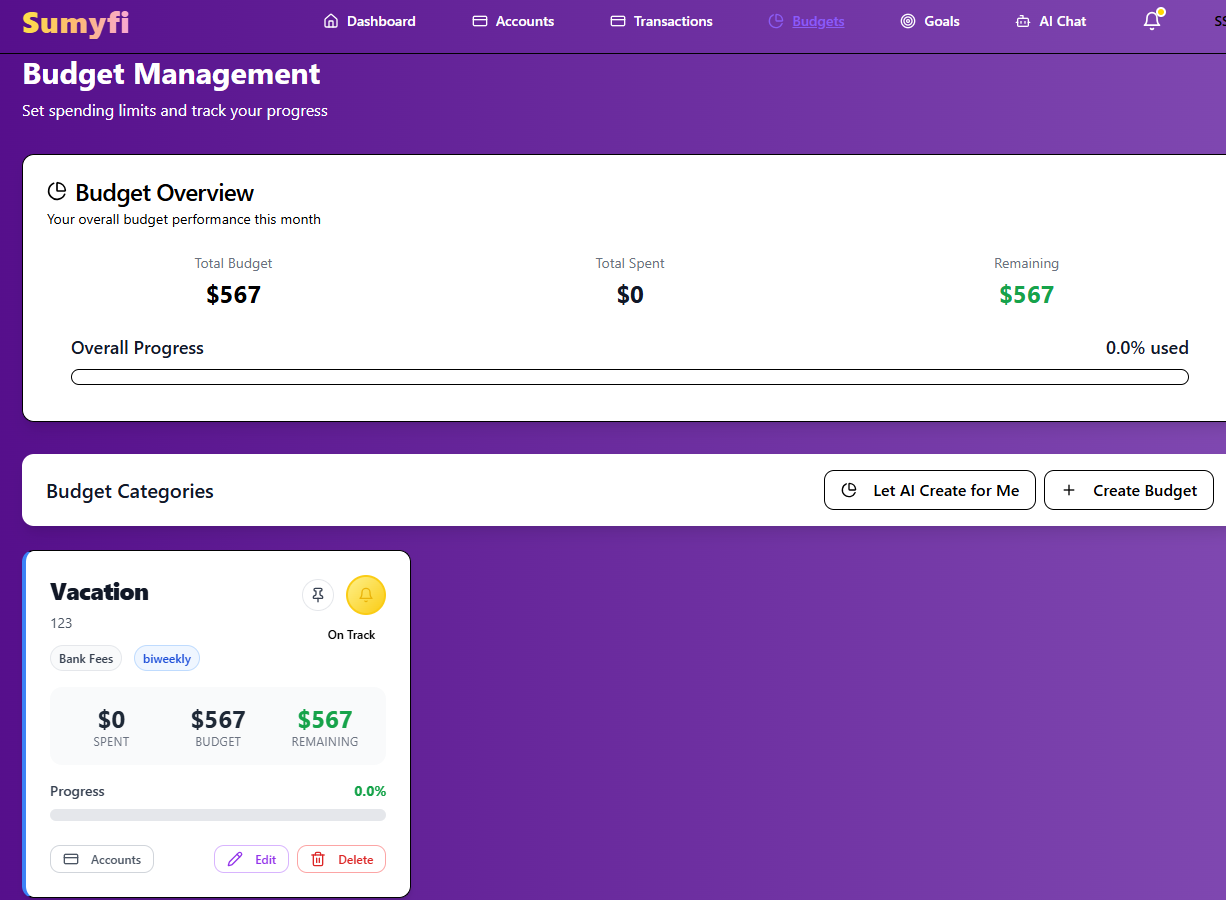

Product screenshots

See the product behind the copy

The screenshots below make the dashboard, accounts, budgeting, AI, reminders, and progress surfaces more concrete for serious buyers.

Comparison pages work better when buyers can actually see the product surface they would be using.

Account coverage and visibility are part of the real comparison, not just the pricing table.

Budgets, goals, and recurring review should be weighed as one system when you compare tools.

Trust surfaces

Trust matters more than surface-level marketing in finance

In a YMYL category, buyers need visible support, security, coverage, and public accountability before they are comfortable connecting money data or acting on product guidance.

Security and privacy

Serious buyers need visible security, privacy, and data-handling pages before they trust a finance product.

Support and help center

A visible help center gives cautious buyers a clearer path before signup.

Institution coverage

Institution coverage matters because connected-account trust is part of the product story for dashboard and aggregation buyers.

Public launch signal

External product-discovery pages add another public trust surface beyond the marketing site itself.

Public roadmap on GitHub

A public roadmap repo gives buyers and readers another transparent trust surface around product direction and external mentions.

Proof block

What former Mint users need before they move on for good

What matters most is whether it proves the buyer can rebuild their weekly money habit on a stronger foundation than the one Mint left behind.

Post-Mint workflow replacement

Weekly review habit rebuilt

Broader system than a legacy reference

"I do not need the closest Mint clone. I need the best system to replace what Mint used to help me do each week."

"The stronger product is the one that rebuilds the habit loop on a better foundation instead of just copying the old reference point."

What matters in practice

What sumyfi vs mint needs to solve in real life

Sumyfi vs Mint matters when the current setup still leaves too much guesswork. People may already have account access, a spreadsheet, a budgeting tool, or a subscription list, but they still do not feel clear on what changed, what is drifting, or what deserves attention first.

The useful solution is the one that turns raw money data into orientation. Sumyfi fits that need by keeping accounts, recurring spending, goals, and planning close enough together that the next decision is easier to make. That also matters in a Mint comparison, where the real choice is whether a narrower tool is enough or a broader system will hold up better over time.

What to look for

- Built around helping people compare Sumyfi against the legacy standard many former Mint users still reference

- Useful for everyday personal finance users

- Designed to reduce fragmented weekly money review

What to test first

The workflow should answer a few important questions quickly

A finance tool earns its place when it helps you answer practical questions without a lot of cleanup. Can you see what changed this week? Can you spot a recurring charge, a balance shift, or a category problem quickly enough to do something about it? Can you move from review into action without opening three more tools?

That is where many products still fall short. They centralize information but leave interpretation scattered. Sumyfi works better when the goal is to keep balances, recurring charges, goals, and next actions close enough together that the review feels usable instead of performative.

What to compare first

How to judge sumyfi vs mint without getting distracted by feature noise

The comparison framework is usually simpler than buyers expect. Look at whether the product makes account visibility easier, whether it explains spending clearly, whether recurring costs and goals stay connected to the rest of the money picture, and whether the workflow still feels manageable after a busy month.

That is where Sumyfi tends to stand out. It is built to help users see the broader financial picture quickly, interpret what changed, and keep planning visible without forcing a dozen separate tools or a heavy maintenance ritual.

What to look for

- Account visibility

- Spending clarity

- Goals and recurring-spend context

- Low-friction repeat use

- Trust and reliability

Why Sumyfi fits

Why Sumyfi makes more sense when the whole system matters

Sumyfi helps with this problem because it is not limited to one narrow money use case. Users can connect accounts, review recurring costs, track goals, and understand changes inside one environment instead of solving one visible symptom while leaving the rest of the system fragmented.

That broader fit matters for everyday personal finance users because the most useful finance app is usually the one that makes the next decision easier without demanding a complicated setup or a spreadsheet mindset. Sumyfi is most useful when the dashboard still helps after the first obvious problem has been handled.

Comparison angle

What matters most when choosing between Sumyfi and Mint

Buyers comparing Sumyfi with Mint are usually not choosing between random apps. They are deciding whether a narrower workflow is enough or whether a broader money system will create more value over time. That matters because the better choice is often the product that stays useful after the first use case is solved.

Sumyfi is strongest when the user wants accounts, spending visibility, goals, and recurring money decisions to reinforce one another instead of splitting across multiple tools. That broader fit is often what makes the difference in a serious comparison search.

Why this comparison still matters

Mint remains the benchmark because it shaped the buyer's habit, not because it is still the best answer

Former Mint users often compare everything to Mint because it defined how they used to review money each week. That makes the comparison emotionally sticky, but the better buying decision is forward-looking. The stronger product should give them a better review loop now, not just a familiar reference point.

Sumyfi is positioned well when the buyer wants to replace Mint with something broader and more durable across budgets, subscriptions, and the rest of the household money routine.

That makes this comparison less about defending against a legacy brand and more about showing that the next system should be genuinely stronger.

Bottom-funnel comparison

The real difference is usually in the workflow, not the feature table

High-intent comparison pages matter because the buyer is usually close to choosing. At that stage, the most useful page is the one that clarifies how each product feels in normal weekly use rather than drowning the user in a long list of loosely comparable features.

The better product for comparing Sumyfi against the legacy standard many former Mint users still reference is often the one that keeps more of the money picture connected after the first use case is solved. That is what determines whether the buyer still feels good about the choice a month later.

What to look for

- The strongest comparison clarifies product philosophy

- Weekly usefulness matters more than isolated feature wins

- The winning app should solve the next problem too

Why buyers switch sides

The decision usually turns on what the buyer wants the whole system to do

A finance comparison rarely ends with one killer feature. Buyers usually change their minds when they see which product better fits the full workflow they want: more structure, more flexibility, broader context, or faster interpretation. The more clearly the comparison communicates that distinction, the more useful it becomes.

That is why connected value often beats isolated polish. The tool that helps the user run the broader system more comfortably is usually the one that feels stronger in hindsight.

Competitive angle

What buyers often underestimate when comparing Sumyfi and Mint

Most buyers initially compare against Mint at the feature level, but the more important difference is usually how the product frames the ongoing financial workflow. A tool can look close on paper and still feel very different once the buyer starts trying to use it weekly for review, planning, and recurring decisions.

The more useful option is usually the one that keeps more of the user's money system coherent after the first immediate use case is handled.

What matters after week one

How to tell whether the workflow will still help after week one

The best test is still a real weekly workflow. If the product makes balances, recurring activity, and next actions easier to review without a lot of cleanup, it is probably a good fit. If it still leaves you stitching the story together manually, the problem is not solved yet.

Sumyfi is strongest when the dashboard, planning layer, and recurring money decisions stay connected. That makes it easier to decide whether the product genuinely improves how you handle comparing Sumyfi against the legacy standard many former Mint users still reference.

Why people hesitate

The biggest buying risk is usually choosing a tool that looks clearer than it feels

Finance buyers often know the category language well enough to compare features, but still struggle to picture what the product will feel like in ordinary use. That uncertainty is rational. A lot of apps sound complete during research and still create too much hidden work once the user tries to rely on them weekly.

The better explanation lowers that uncertainty by showing how the workflow behaves under normal life pressure. That is usually more persuasive than adding another layer of generic claims.

Decision speed

What makes a tool easier to act on quickly

People search these categories because they want relief from uncertainty, drift, or unnecessary effort. The product that wins is usually the one that makes the next decision easier once the user opens it. If the app still requires a lot of interpretation or a second system to translate the data, its value plateaus quickly.

That is why connected design matters. When visibility, recurring patterns, and planning context stay close together, the app becomes easier to trust and easier to keep using.

Search intent

Why this is usually a serious search and not casual browsing

Searches like sumyfi vs mint usually come from users who already feel some friction in the current setup. They are not trying to learn whether finance apps exist. They are trying to decide which product will reduce confusion, lower maintenance, or create a better money habit quickly enough to justify the switch.

That makes specificity important. A useful guide helps users see why Sumyfi is relevant to comparing Sumyfi against the legacy standard many former Mint users still reference without pretending every buyer wants exactly the same kind of workflow.

FAQs

Frequently asked questions about sumyfi vs mint

Is Sumyfi really a strong option for sumyfi vs mint?

Yes, especially if the real goal behind the search is reducing fragmentation. Sumyfi is strongest for users who want connected accounts, clear budgeting, visible goals, recurring-spend awareness, and modern AI-assisted explanations in one place rather than separate disconnected tools.

What matters most when comparing options for sumyfi vs mint?

Account connectivity, spending clarity, recurring-charge visibility, budgeting depth, goal support, trust posture, and ease of repeat use matter most. Those factors influence whether the tool becomes part of your real routine or remains a short-lived experiment.

How does Sumyfi help people researching sumyfi vs mint day to day?

Sumyfi helps by keeping the wider money picture visible for people trying to compare Sumyfi against the legacy standard many former Mint users still reference. That makes it easier to understand tradeoffs, track progress, and act on recurring patterns without rebuilding the context in separate tools.

What makes a finance app easier to keep using over time?

Low-friction review loops matter most. If the dashboard helps you connect accounts, understand patterns quickly, and take the next action without extensive manual cleanup, you are much more likely to stay engaged. That ongoing usability matters more than a long feature list.

Who is Sumyfi vs Mint usually best for?

It is usually best for everyday personal finance users who want clearer financial visibility without building a heavy manual system. Sumyfi is strongest when the user wants practical weekly clarity more than niche complexity for its own sake.

Supporting articles

Read related explainers before you commit

These blog articles add broader context around budgeting habits, expense tracking, automation, and product-fit questions so readers can keep digging into the same decision from a few useful angles.

Blog explainer

Best Budgeting App in 2026

A wider market explainer that helps buyers compare product philosophy, not only features.

Read article

Blog explainer

Best Budget App in Canada

Useful when comparisons overlap with Canada-specific product-fit questions.

Read article

Blog explainer

Best Budget App for Couples

Useful when the comparison is really about shared-expense workflow and visibility.

Read article

Keep exploring

Continue the same decision journey

These related guides keep the comparison useful for both visitors and search engines by routing buyers into the next relevant comparison, budgeting, dashboard, or net-worth question.

Related guide

How to Switch from Mint

moving from Mint to a cleaner financial tracking system for accounts, subscriptions, savings goals, and weekly money review

Read How to Switch from Mint

Related guide

Connect All Bank Accounts in One App

bringing checking, savings, credit cards, and investment accounts into one unified dashboard

Read Connect All Bank Accounts in One App

Related guide

Best Subscription Tracker App

finding recurring charges, monitoring bills, and reducing waste from forgotten subscriptions

Read Best Subscription Tracker App

Related guide

Best Savings Tracking Software

tracking savings goals, progress, and recurring contributions inside a broader financial dashboard

Read Best Savings Tracking Software

Related guide

AI Personal Finance App

using AI to explain spending, prioritize goals, and simplify money decisions

Read AI Personal Finance App

Related guide

Sumyfi vs Rocket Money

comparing a broader finance dashboard against a tool many shoppers associate with subscription visibility

Read Sumyfi vs Rocket Money

Topic cluster

Keep exploring the same decision journey

More Mint comparison searches

Keep exploring nearby buyer-intent pages for people comparing Sumyfi with Mint and similar alternatives.

Comparison Search

Sumyfi vs Rocket Money

comparing a broader finance dashboard against a tool many shoppers associate with subscription visibility

Comparison Search

Sumyfi vs Monarch

comparing Sumyfi with another premium-style personal finance experience

Comparison Search

Sumyfi vs Monarch Money

comparing Sumyfi against a popular premium-style money dashboard

Comparison Search

Sumyfi vs YNAB

comparing an all-in-one finance dashboard with a budgeting-first workflow

Related use cases and adjacent searches

Branch into nearby searches that tend to appear in the same decision journey, from alternatives to dashboards to budgeting help.

Comparison Search

Sumyfi vs Copilot Money

comparing Sumyfi against another modern dashboard-focused money app

Comparison Search

Sumyfi vs Empower

comparing Sumyfi against a platform many shoppers consider for high-level financial visibility

Comparison Search

Sumyfi vs Credit Karma

comparing broader money management against a credit-focused financial tool

Guide hub

Browse the full Sumyfi topic cluster

Move from one question to the next through budgeting, dashboard, subscription, AI, and comparison guides that support the same decision journey.